The Do's and Don'ts of Hiring a Banker When Selling Your Business

- Why founders need the support of an investment bank when selling their business

- What founders should and shouldn't do when evaluating banks, negotiating fees, and determining the best time to hire

Selling a business is a complex process requiring hard-won experience and specialized expertise. As such, founders do well to engage the right investment banker, at the right time, and with the right compensation structure in order to successfully sell their business.

Read on to learn why you should hire an investment banker and the do’s and don’ts of doing so.

Why you need to hire an investment bank as a founder

Sophisticated players in the M&A markets (i.e. institutional investors and strategic buyers) buy and sell businesses over and over again, and yet they rely on investment banks to advise them. Why do these players hire help if they have so much experience? Because their experience makes them well aware of the complexities of a transaction.

Buying and selling businesses is a volatile process that requires significant resources to execute well, so sophisticated players hire support. Founders who recognize this truth take similar action, hiring an investment bank to push the deal process in their favor and dedicate the necessary resources to run a competitive process.

Reason #1 to hire a banker: Businesses are volatile assets

The price buyers will pay for businesses is extremely elastic, meaning the price buyers are willing to pay varies greatly from one buyer to the next. In transactions we have run, the value of the highest bid has been 5-7x the value of the lowest bid.

Bankers use this elasticity to the benefit of founders by running a structured transaction process that includes players that pay premiums.

Founders who elect to run their own transaction often miss out on attractive multiples due to a lack of experience selling businesses. Bankers, on the other hand, understand the buyer and investor landscape and as such they know:

- Which buyers to include in a process based on willingness to pay

- How to position the business in the most favorable light possible to boost multiples

Reason #2 to hire a banker: Businesses require significant resources to sell correctly

On the sell-side, the best outcomes for founders come from running a competitive process with a lot of buyers. Given that managing relationships with 30+ buyers is a huge task, founders that try to run a transaction on their own end up getting distracted from business operations. As a result, their focus on selling the business comes at the expense of business performance. In such scenarios, founders often settle for the first buyer who puts forth a term sheet.

The beauty of hiring an investment bank is that they can focus solely on the transaction while you focus on the business. (The bankers at Vista Point Advisors dedicate 400+ hours of work per transaction.) By focusing on your business, you can take your business to market with a message of continuous growth and high performance.

If you’re still on the fence about the value of an investment banker, consider the value of your business. As a founder, your equity is likely the most valuable asset you own, even more than your own home. Is saving the fee from an investment bank worth the risk of an ill-run transaction, especially when you consider the enterprise value a bank can add by running a competitive process?

Hiring a banker will get you a better deal. But hiring a good banker will get you an even better deal. Consider the below do’s and don’ts when engaging with investment banks.

The Do’s and Don’ts of Evaluating an Investment Bank

Not all investment banks are made equal. When looking at each bank, you will want to consider:

- Sector & product expertise

- Average deal size and bank size

- Bankers on the deal

- Potential conflicts of interest

Sector & product expertise

While this point may seem obvious, do make sure your banker has the right expertise to sell a business in your sector (e.g. software, internet, etc.) and in your desired transaction type (e.g. M&A, private equity).

For example, if a banker has done M&A transactions in the edTech software sector but has never done a capital raise with private equity, you shouldn’t expect them to do a good job in the private equity product group.

Do verify sector & product expertise by checking out the bank’s transaction history (often called "tombstones"). As you do so, do ask what role the bank played in the transaction. Banks will frequently cite deals they didn’t act as an exclusive advisor on—they may have simply written a fairness opinion or even worse, they didn’t even work on the deal!

Do consider nuances in sector expertise. For example, consider the subtle difference between banks that advise on healthcare services vs. HCIT.

Some bankers with sector expertise (especially the larger banks) will pitch "relationship access" as a value add, suggesting that their connections will make running a transaction easier.

Do question the value of that purported "relationship access." In the modern era where LinkedIn makes connecting with buyers easy and many buyers will reach out to you directly, a banker’s “Rolodex” is significantly less important than other factors, such as:

- How much experience they have in the sector

- How competitive of a process they can run

Lastly, don’t forget to scrutinize the type of buyers a bank tends to close with. Outcomes for founders vary greatly depending on if a bank works with value-seeking buyers vs. buyers who pay premiums.

Average deal size and bank size

Do review each bank’s average deal size compared to the size of your deal. Bankers (especially senior bankers) tend to focus their time on the largest deals with the most lucrative fees. If your deal is small compared to others the bank is transacting, you may not get the attention your deal needs to reach an optimal outcome.

Bank size should also play a role in who you select. Don’t choose a bank that’s too big for your deal size, as you will likely be relegated to the bottom of the priority list.

Generally, large banks will pitch a "full suite" of services that clients can draw upon (e.g. ECM, DCM, advisory, research, sales and trading, etc.). Don’t get drawn in by the full suite, as most of these products will be irrelevant to your transaction.

At the same time, don’t pick a bank that’s too small. While boutique investment banks often have more specialized expertise, in some cases small banks opt out of registering their business with the SEC and FINRA due to the costly and time-consuming regulatory process. Unregistered banks are limited in the types of transactions they can run (based on SEC regulation), which limits your options as a founder and stifles a competitive process. In the worst case scenario, a deal could unravel because a bank isn’t registered to conduct that type of transaction.

Bankers on the deal

Banks are only as good as the bankers who work there, or rather, the bankers who work on your deal.

Many banks pitch "senior attention, " but often just bring in the senior bankers for a pitch before delegating to junior bankers to execute the transaction. Do verify which bankers will be handling your deal. A good way to do so is through reference calls with the bank’s former/current clients, in which you can ask:

- How responsive the bankers were after a signed engagement letter compared to before

- What each team member contributed

- How many active deals the current team is working on

Like other service professionals, bankers frequently jump ship to other firms and opportunities. Do conduct diligence on how long a banker has been with their current firm and whether he or she is likely to leave. Be extra cautious during bonus season (generally at the end of Q2 and Q4) as these are the times when bankers tend to swap firms.

If you’re worried about losing your banker to another firm, do consider including a key man provision in your engagement letter. Said provision will nullify your engagement if that key man is not available to work your transaction.

That being said, investment banking is a team sport, built up of analysts, associates, VPs, and principals. The best teams have worked together for some time, so do evaluate how long the team has been together.

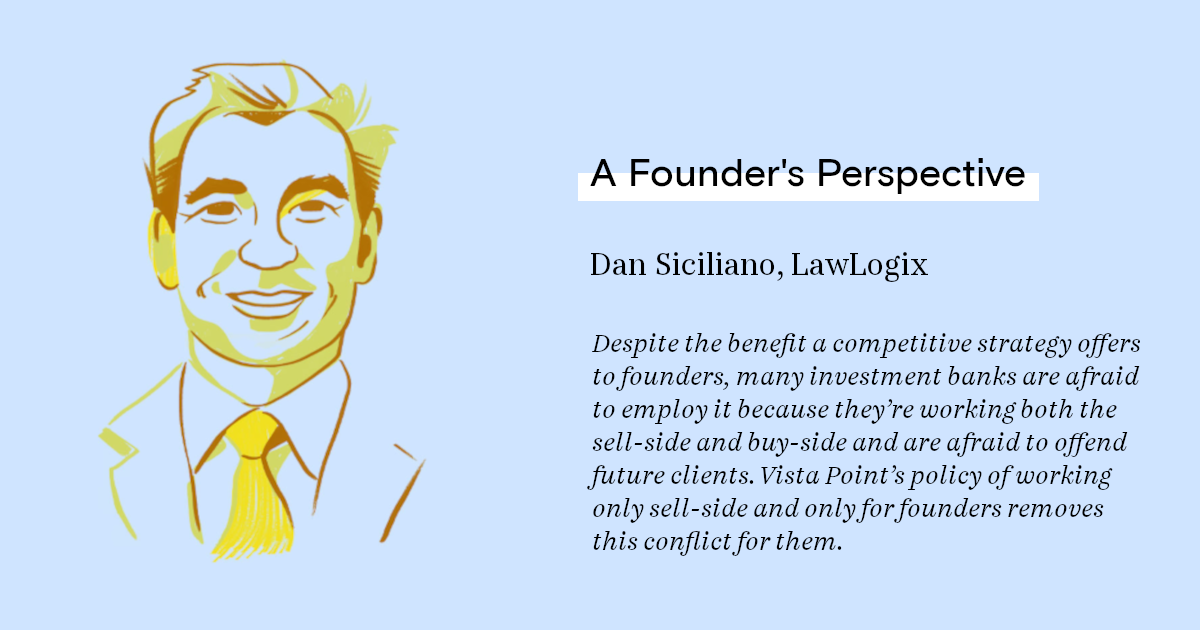

Potential conflicts of interest

In some cases, bankers will work both the buy-side and sell-side, meaning for one deal they’ll advise a buyer and the next they’ll advise a seller. Doing so can create serious conflicts of interest when a banker represents a founder.

Don’t work with bankers who work both sides of the table, as these bankers are highly incentivized to give concessions to repeat buyers and investors who are current or future clients.

To be explicit, as a founder on the sell-side, you’re likely to only work with a bank once, and bankers know that. As such, if conflicted bankers have an opportunity to secure the good graces of a buyer (i.e. a potential client who represents long-term recurring revenue in the form of acquisitions, divestitures, IPOs, follow-on debt & equity financings, portfolio company work, and more), those bankers may give special privileges to that buyer at the expense of the founder they represent.

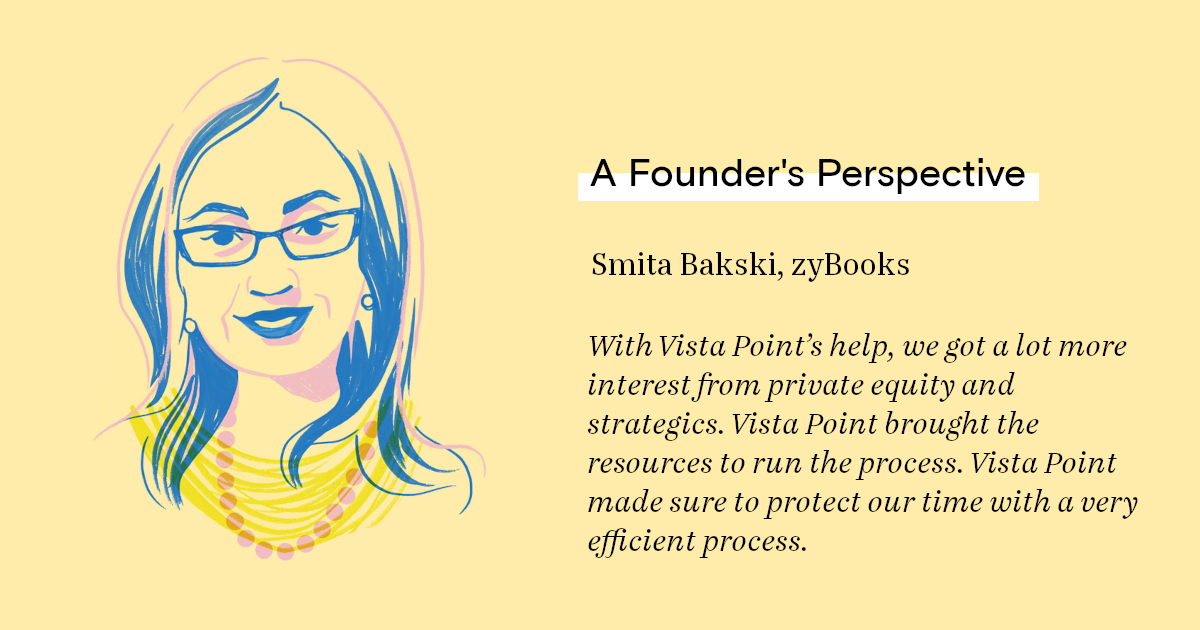

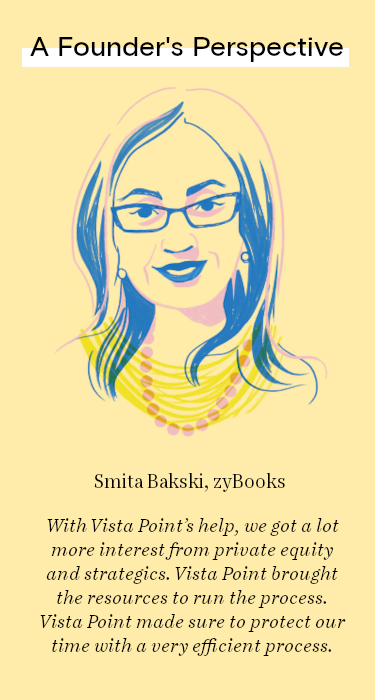

Do find an investment bank that has no conflicts of interest (i.e. they only represent founders on the sell-side). An unconflicted investment bank is able to have tough negotiations with buyers to the benefit of founders because the bankers don’t have to worry about upsetting relationships with future clients.

The Do’s and Don’ts of Negotiating Fees with an Investment Bank

Once you’ve decided which investment bank you want to work with, you will have to negotiate the bank’s fees. Correctly negotiating fees is vital to the success of a transaction, as fees create incentives for banker behavior. An incorrect fee structure could create the wrong incentives for bankers.

For example, consider a basic fee structure where a banker is compensated for a high valuation. While this structure may seem straightforward and aligned, achieving a high valuation at all costs isn’t ideal under the following circumstances:

- The buyer offers a high valuation but requires investor-friendly security structures and protective provisions

- The buyer ties up a large portion of enterprise value in earnouts that are contingent on performance

- The buyer offers a high valuation, but there is a high risk they won’t close in diligence

In each of the above cases, you would be better off taking a lower valuation, but your banker may advise otherwise if they’re compensated for a high valuation.

Do evaluate the ways a fee structure can affect incentives. A good valuation isn’t the only factor to consider—you likely have a lot of goals for the business other than the financial rewards. Don’t ignore non-valuation related objectives, such as:

- Security structures

- Cash at close/earnout structures

- Founder roles post-transaction

- Treatment of cash/debt in the business

- Treatment of insider investments

- M&A insurance

- Responsibility for funds flow documentation

- And others

The Do’s and Don’ts of When to Hire an Investment Bank

When is the right time to hire an investment bank? Could you possibly hire a banker too early?

Yes, you can hire a banker too early. Generally, bankers like to pitch the concept of early engagement, saying they would like to introduce your company to potential buyers then slowly mature those relationships over several years.

The primary issue with this approach is that your business today will be significantly different from what it will be in the future.

At a minimum, you’ll be wasting time coordinating with a banker how to sell your business for years while the business evolves into something completely new. At worst, your banker could completely misrepresent your business or set up inaccurate expectations that become a negative hurdle when you take the business to market. Don’t buy into the "early introduction" approach.

You don’t want to involve an investment bank too early. But is it possible to bring on an investment bank too late?

Unless you’re already in exclusivity with a buyer, the answer is no. At Vista Point Advisors, we’ve had clients hire us as late as the final steps in a purchase agreement (after an exclusivity period expired) due to difficulties they had dealing with a buyer.

Until a transaction is closed, every negotiation, term, or dollar amount is non-binding. Don’t feel like you’re too late in a process to build leverage through competition (whether real or perceived).

So when is the ideal time to engage an investment bank? As a full process takes around 4-6 months to complete, do bring in a banker roughly 6 months before you would like to close. Much of a banker’s time and resources will be spent preparing marketing materials—especially if you’ve never gone through a large M&A process before and therefore might not have the right data to run a fulsome process.

Even in situations where data is readily available, nearly 100% of the time a banker will have to gather, analyze, and present the data in a way buyers will easily understand.

For example, in a SaaS business a banker may have to tie revenue by customer by product by month to the income statement and note where inconsistencies exist.

Giving a banker just enough time to run a robust process will help you achieve a good time-to-close and a good outcome for you as a founder.

Hire the Right Banker. Yield a Great Outcome.

Who you choose to represent you when selling your business will greatly influence your final outcome. A banker in the right sector, with the right experience, fee structure, and timing, will help you turn a good outcome into a great one.