Why You Need an Unconflicted Banker to Sell Your Business

- How the incentives between investment banks and founders can be misaligned

- Techniques to identify an unconflicted investment bank

When you hire an investment banker to help you sell your business, incentives play a huge role in determining whether or not that banker is motivated to drive the best outcome.

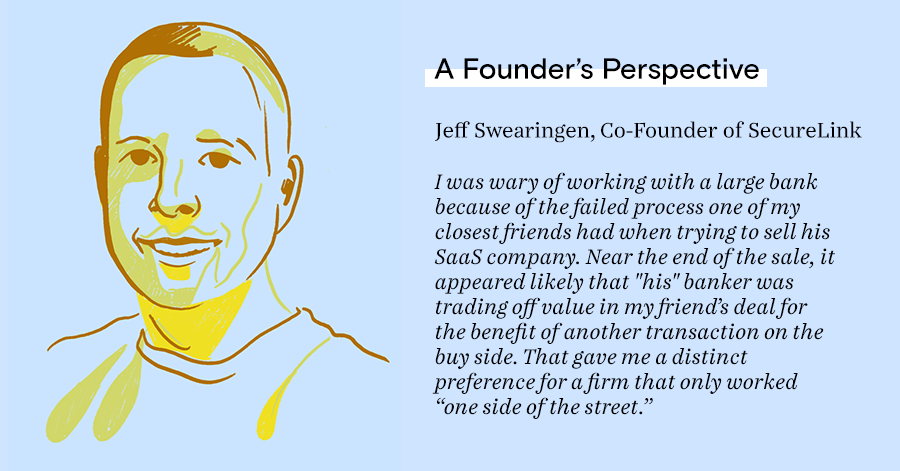

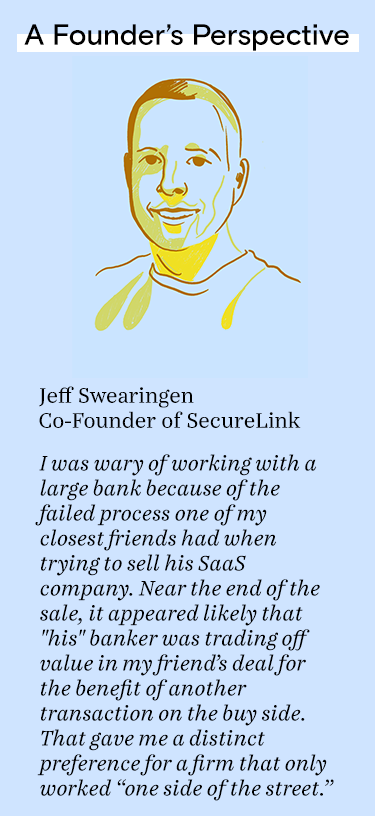

Have you ever considered that a banker’s incentives might be the opposite of yours? This seems odd, considering you’re paying the banker to represent you. But in many cases an investment banker has a conflict of interest that can negatively affect your outcome as a founder. Here’s how that happens.

What Makes an Investment Banker Conflicted?

Sophisticated players in any industry generally do what’s in their best interest, and investment bankers are no exception. If your banker’s interests aren’t aligned with yours, you can be sure they’ll play to their own interests over yours.

Three primary scenarios under which a banker may have a conflict of interest include:

- When the banker works as both a buy-side and sell-side advisor

- When the investment banker does sell-side work for private equity firms or strategic buyers

- When the investment bank requires co-investment

The problem with a banker working both buy-side and sell-side

Most investment bankers take on both sell-side and buy-side transactions, meaning that they’ll advise a buyer/investor on the buy-side for one transaction and a founder on the sell-side in another transaction.

These investment banks try to portray working on both sides as a positive, because their "experience on the buy-side allows them to develop better relationships with potential buyers." This argument, however, overlooks an important motivator for investment banks: fees.

Private equity firms and strategic buyers are repeat players in the market and they pay Wall Street hundreds of millions in fees. If investment bankers can manipulate a sale to benefit a current or potential buy-side client, they may be able to secure future revenue.

For example:

- If an advisor is working the sell-side and one of their repeat buyer clients is in the buyer pool, they are incented to favor that buyer to protect the recurring revenue they receive from advising that client’s buy-side transactions.

- If an advisor is working the sell-side and a private equity firm is in the running, they are incented to favor the private equity firm over other buyers because they know the PE will sell the company in 3-5 years and the advisor might be able to secure an engagement for that future sale now or secure an engagement to sell another portfolio company of the PE firm.

The problem with a banker doing sell-side for private equity firms or strategic buyers

A similar conflict arises when an investment banker works on the sell-side for a portfolio company of a private equity firm or large strategic buyer.

In the case where a banker is working for a founder and one of the potential buyers in the running is also a current client of the banker, the banker has an incentive to favor that buyer to strengthen the relationship and ensure future revenue.

In any situation where a banker has an incentive to favor a certain buyer outside of the best interests of the founder, the outcomes likely won’t fall in favor of the founder.

The problem with an investment bank requiring co-investment

Some investment banks will insist on having the ability to co-invest or essentially "buy" a part of the business at the same price as the buyers/investors. This may be a requirement in their engagement letter, and they may even try to portray this as a positive by saying they are “aligned” with you.

However, exactly the opposite is true. By introducing this option in the engagement letter, bankers now have an incentive to sell the business at a reasonable if not low price so they can capture the extra value in the sale.

In addition, co-investment also potentially limits the buyers/investors that would participate in this type of transaction as the majority of buyers/investors do not want the bank owning a piece of the business post-close. Less buyers means less competition, which means a worse outcome for the founder.

Ways a Conflicted Advisor Can Misguide Your Transaction

Conflicted advisors have many ways of manipulating a transaction in their favor, including:

- Suggesting you sidestep the deal process for a buyer or encouraging a buyer to preempt the process

- Giving one buyer or buyer group more access to information and more time with management

- Advising you to move into exclusivity with one specific party too early in the process when other players have signaled they might pay more or will have a quicker time to close

- Moving on the buyer’s timeline instead of yours

- Limiting the buyer pool to ensure favorable terms for the advisor’s preferred buyer

- Moving the process too quickly to prohibit strategic involvement*

*Note: Strategic buyers move a little slower up front as they:

- Need to receive feedback and buy-in from more internal stakeholders.

- Take more time reviewing NDAs

- Have operational day jobs to manage

A good investment banker will make sure to give strategic buyers enough time to evaluate the opportunity so that private equity firms don’t choke those buyers out of the competition.

How to Detect If An Investment Banker Is Conflicted

You obviously don’t want to wait until after signing an engagement letter to discover that your advisor is conflicted. To detect upfront if an advisor might have a conflict:

Ask what percent of the investment bank’s revenue comes from buy-side engagements. If the percent is high, you know they have incentive to favor buyers.

Ask if the investment bank works as sell-side advisors on any portfolio companies of firms that could also be your buyers. If so, there might be a conflict.

Look to see how many times the investment bank has sold a company to a private equity firm and then represented a portfolio company of that same investor in short order. (This is a common quid pro quo in investment banking, where the PE will hire the banker to sell one of their companies if the banker gives them an unfair advantage on a company they are trying to buy from the banker.)

If you notice any red flags in these areas, you’re better off choosing a different investment bank to run your transaction.

What an Unconflicted Investment Banker Looks Like

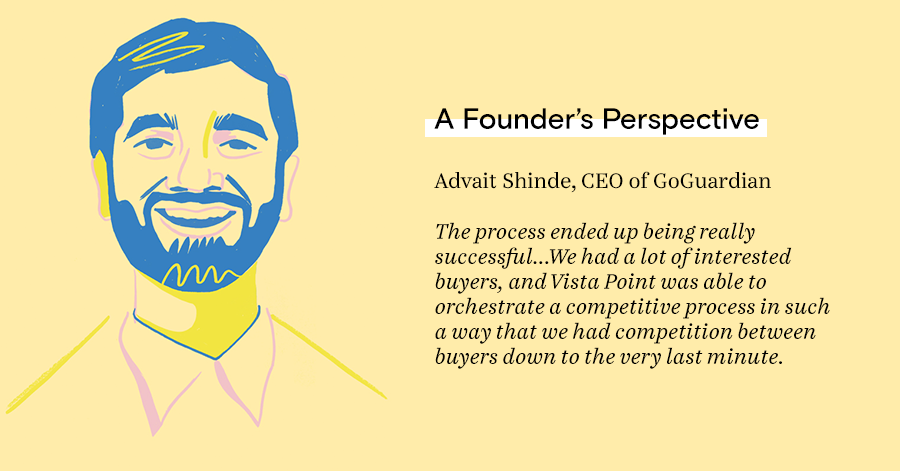

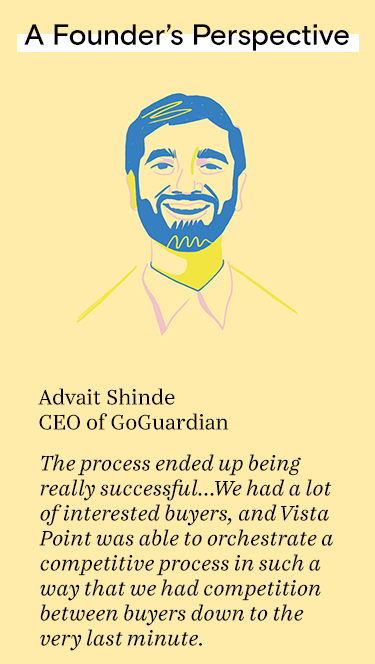

You should hire a banker that does not have an interest in who prevails in your process. The banker should look at the buyer universe as a blank canvas and focus on maximizing your interests and executing the most competitive process possible.

Some indicators that a banker will be unconflicted are:

- The banker works sell-side only. By working exclusively on the sell-side, an investment banker doesn’t create incentives to favor any specific buyer. The only relationship a banker should have with buyers is presenting them with good companies while identifying who will pay the most and offer the best terms to sellers.

- The banker doesn’t advise portfolio companies of potential buyers, whether on the buy-side or sell-side.

- The incentives are truly aligned, with the banker’s outcome directly correlated with the outcome of your deal.

At Vista Point Advisors, we believe every founder deserves an unconflicted advisor that is fully aligned with you to navigate the M&A process and deliver the optimal outcome. Because we are unconflicted, we can be the type of advisor who you can feel comfortable listening to because we’re fully aligned with your goals to reach the best possible outcome.