The Investment Banking Process When Selling Your Company

A breakdown of the stages in the deal process, including:

- Pre-Marketing

- Marketing

- Diligence

- Documentation

The ultimate goal of selling your business is to maximize value for you as the founder.

An investment banker can help you maximize value by bringing their expertise to the entire deal process. They do so by helping you ensure the deal remains:

- Competitive. Negotiating in tandem with several interested parties drives valuations up and helps you negotiate out unfavorable terms.

- Positioned. When presenting, you want to make sure your metrics and company descriptions frame your company in the most positive way possible for buyers.

- Efficient. The swifter you can reach an optimal outcome, the better.

- Organized. Setting clear milestones for the process helps ensure quality from bidding parties.

- Confidential. Confidentiality protects your business from revealing proprietary information to the wrong party.

When working through an investment banker, the deal process typically takes somewhere between 4-6 months, though in some cases can move as quickly as 3 months. Here is what the deal process typically looks like:

Stage 1: Pre-Marketing

Length: 2-4 Weeks

Before you can take your business to market, you and your investment banker will need to make the necessary preparations, including:

- Cleaning up your financials

- Generating marketing materials

- Creating your buyer/investor list

Cleaning up your financials

Most of the effort spent in this stage is focused on ensuring the company’s internal financials and customer data all neatly tie together and that this information is easy for buyers to audit later on in the process.

Though a company's financials aren't expected to be 100% GAAP, all revenue and expenses should be easily auditable back to original sources.

Generating marketing materials

Once your financials are cleaned up, you and your banker will create a Confidential Information Presentation (CIP). Your CIP will be a ~30-page deck laying out key business metrics and explanations for buyers to evaluate your business at a high level.

The general sections within the CIP are:

- Historical financials and near-term forecast

- Customer analyses (e.g. revenue by product by customer, retention analysis, revenue composition analysis, etc.)

- Product information, functionality, and infrastructure

- Market overview and the company’s growth opportunities

- Organizational/structural information and cap table

Many of the analyses you include in your CIP will also appear in your management presentation deck. This deck is the lens through which buyers will see your business and is how you will make your first impression with buyers. As such, this deck is a critical document and you should rely on your banker’s expertise when building it out.

Your banker will also help build out a transaction teaser, which is a one-page, anonymous summary about your company to garner interest from potential buyers before they receive the full CIP upon signing an NDA.

Creating your buyer/investor list

The buyer list should be a collaborative effort between the banker and you, the selling company.

The banker should take input from the founder on who the founder would like to include or exclude as a potential buyer. In addition, the banker should be able to bring additional buyers to the table through their knowledge of the sector and network of past buyers/investors.

Founders and their bankers should discuss how to approach each potential buyer to take into account preexisting relationships, competitive sensitivities, and custom nuances to each party. For example, if a founder has an existing customer who could be a buyer, then it may make sense to have the founder reach out directly to initiate the conversation.

Another issue to cover as you create your list is letting your investment banker know whether a proposed buyer could pose a competitive threat. Such companies could use the knowledge of your sale against you by notifying your partners or customers to weaken your relationship with them.

![Once we were ready to take the business to market, together [Vista Point and I] made a list of potential interested parties, rather than just talk to the people who had been mulling around kicking tires. Then they set a date for the sale. And that lit a](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1330/Chris_Bond_2_Dekstop.png)

![Once we were ready to take the business to market, together [Vista Point and I] made a list of potential interested parties, rather than just talk to the people who had been mulling around kicking tires. Then they set a date for the sale. And that lit a](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1331/Chris_Bond_2_Mobile.png)

Summary of Pre-Marketing

The responsibilities of the founder and the investment banker in this phase of the deal process are as follows:

Investment Banker

- Conduct business and financial diligence to gain a strong understanding of the business

- Create financial projections

- Draft a transaction teaser

- Draft the CIP and management presentation

- Construct an initial buyer list

Founder

- Provide materials for the banker to finalize business and financial diligence

- Review initial buyer list and identify any competitively sensitive buyers

- Review CIP and management presentation

- Verify transaction NDA

Stage 2: Marketing

Length: 4-8 weeks

When the time comes to take your business to market, you will use the marketing materials you prepared together with your investment banker to frame your business for buyers. The activities you’ll engage with in this stage are as follows:

- Make initial contact with buyers

- Execute NDAs and send the CIP to interested buyers

- Qualify buyers

- Conduct management presentations

- Distribute process letters for next steps

- Receive first-round bids

Make initial contact with buyers

Either you or your investment banker will make initial contact with C-suite management and/or corporate development reps at the target buying company or private equity firm. Initial contact usually involves sharing the anonymous teaser, followed by an opportunity for the buyer to ask a few questions.

Execute NDAs and send the CIP to interested buyers

Once a buyer expresses interest, the banker sends over a non-disclosure agreement (NDA) for the buyer, prohibiting the buyer from disclosing the identity of the selling company and the information contained in the CIP.

Buyers will often have questions for the investment bank after reviewing the CIP. At Vista Point Advisors, we try to keep the back-and-forth of questions to a minimum at this point until we have identified the buyers who have real interest in the opportunity and are qualified for the transaction.

Qualify buyers

In order to save time and resources, your investment banker will take some time to vet buyers on the list to ensure they meet the minimum qualifications of a buyer. Some dimensions on which to qualify a buyer include:

- Overall interest

- Historical experience in the sector

- Financial capacity to make the purchase

- Track record of M&A and historical bidding

Conduct management presentations

For those buyers who qualify, the banker will schedule 1-hour management presentations over conference call for the founder and their management team to review key concepts from the CIP and field any questions from the buyer.

These presentations are a time for founders and bankers to further narrow down the buyer list based on interest level. Generally, management will participate in 10-20 presentations, depending on the situation. To help management prepare, the banker will schedule a practice session in which the banker will ask common questions and ensure the presentation is consistent with the CIP and other discussions with buyers.

Distribute process letters for next steps

Following the presentations, the banker will share with interested buyers a process letter that outlines the information the buyer should provide in their first round bid in the form of an indication of interest (IOI), as well as timelines for when they should submit their bid. Some of the information a buyer should include in their IOI include:

- Proposed bid

- Basic details of a proposed transaction structure

- Diligence topics they would like to address in the next phase

Receive first-round bids

Buyers then share their bids directly with the banker, who evaluates them in comparison with the other bids to determine which parties the selling company should continue engaging with.

Summary of Marketing

The responsibilities of the founder and the investment banker in this phase of the deal process are as follows:

Investment Banker

- Reach out to buyers with a transaction teaser (when appropriate)

- Execute NDAs

- Send out CIPs once NDAs are fulfilled

- Schedule management presentations for qualified buyers

- Distribute process letters for next steps

- Receive bids and IOIs

Founder

- Conduct management presentations

Stage 3: Diligence

Length: 3-6 weeks

After receiving first-round bids, together founders and bankers will narrow down the buyer list to 3-5 potential buyers. These buyers will then have the opportunity to review additional company information through a private data room during the diligence stage. This stage carries out as follows:

- Accrue and open a data room

- Schedule half-day, on-site meetings

- Accept second-round bids

Accrue and open a data room

To conduct their diligence, buyers will need access to information beyond what’s included in the CIP. A data room is an online portal for sharing information in a confidential manner so buyers can access the information they need to evaluate a company.

The investment banker will be responsible for setting up the data room, and may even start adding information during stage 2 as they gather information for the CIP. Some common items a banker will include in the data room are:

- Employee census and historical compensation data

- Organizational and reporting structure and documents

- Sales team and pipeline data

- Forecast model

- Lease details

- Key partner agreements

- Marketing spend and productivity data

- Customer contracts

- Employment agreements

- Option certificates

- Other items

Schedule half-day, on-site meetings

Once buyers have had a chance to review the information in the data room, the investment banker will set up half-day meetings for the buyer to meet the management team in person.

Ideally these meetings will be on-site at the selling company’s headquarters. In cases where management is sensitive to having buyers present during the work day, the meeting can take place at a nearby facility with a potential walkthrough in the evening.

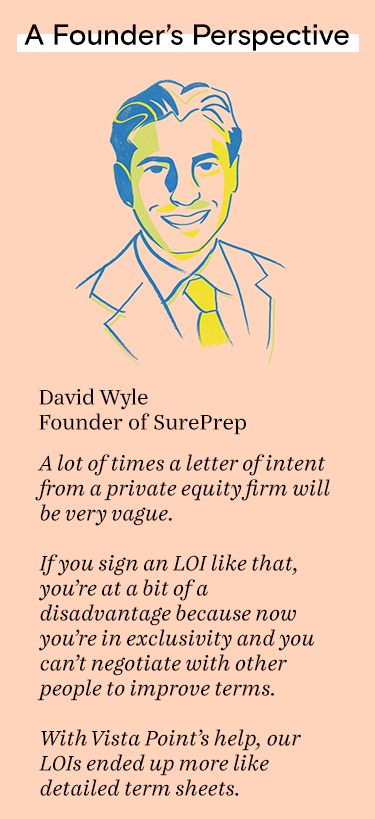

Accept second-round bids

With access to more information and an opportunity to meet with management, buyers will be equipped to make a more detailed second round bid in the form of a letter of intent (LOI), or "term sheet." In the event there is no clear winner, the banker should ask buyers to show stronger closing commitment (such as finalizing quality of earnings audits or drafting a purchase agreement), as well as increase valuation as everything is still non-binding.

Summary of Diligence

The responsibilities of the founder and the investment banker in this phase of the deal process are as follows:

Investment Banker

- Analyze initial and second-round bids and recommend strategies to improve terms

- Create and manage the data room including all access privileges

- Add relevant diligence information to the data room

- Organize and attend on-site meetings

Founder

- Provide diligence information

- Make relevant personnel available to the banker for questions

- Evaluate bids along with banker

Stage 4: Documentation

Length: 3-6 weeks

Following second-round bids, the selling company and their banker should be able to select a buyer from among the finalists to begin the closing steps. These steps under the documentation stage are as follows:

- Finalize third-party diligence under exclusivity

- Review the proposed purchase agreement

- Create a funds flow spreadsheet

- Sign the purchase agreement and initiate wire transfers

Finalize third-party diligence under exclusivity

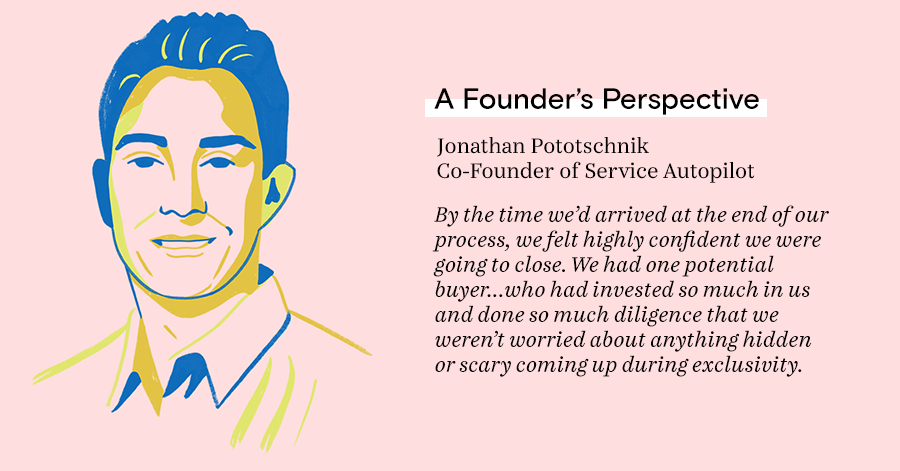

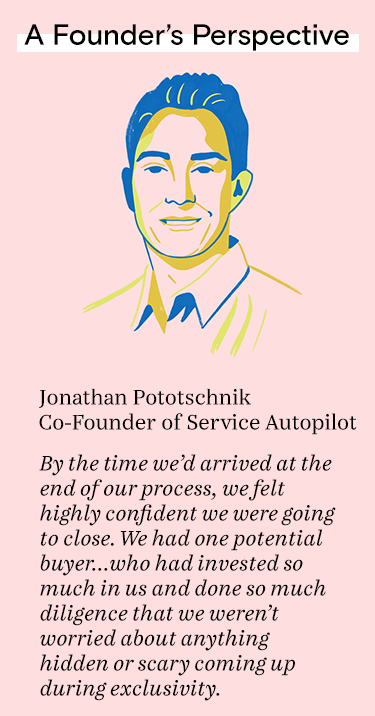

Once the final buyer is selected, the investment banker will open a relatively short window of exclusivity (~30 days) where the selling company agrees to pause conversations with other buyers. Buyers require this exclusivity period as they will have to expend significant resources to consummate the transaction.

During the exclusivity period, the selected buyer will be able to finalize third-party diligence, such as quality of earnings audits, technology review, and legal review, as well as draft their final purchase agreement.

Review the proposed purchase agreement

While most of the terms of the agreement should be tied up by now, your banker will assist you in conducting final negotiations with the buyer to incrementally maximize your value in the transaction.

The banker will also assist in the preparation of the disclosure schedule, which discloses any additional and relevant information about the company that are too extensive to include directly in the purchase agreement, such as contracts, court injunctions, competitive agreements, etc. The selling company’s legal counsel will take the lead on preparing the disclosure schedule.

Create a funds flow spreadsheet

A funds flow spreadsheet is a document outlining the eventual transfer of funds when the transaction closes. These spreadsheets are extensive and complicated, detailing the source of all funds, who receives those funds, the accounts the funds come from (including bank account and routing numbers), and other information all down to the penny.

In situations where companies have raised prior rounds of even minimal capital, the banker will carefully examine the various security classes to uncover the specific payment mechanics and details that must be adhered to (commonly referred to as the "cap table waterfall").

When the time comes to create the funds flow sheet, you’ll be happy you hired an investment banker.

Sign the purchase agreement and initiate wire transfers

Once the purchase agreement is finalized and all parties are content, the selling company and the buyer will sign the agreement and initiate wire transfers. These transfers may happen all at once with the signing of the agreement or may be staggered if there are additional steps to fulfill.

Summary of Documentation

The responsibilities of the founder and the investment banker in this phase of the deal process are as follows:

Investment Banker

- Review and negotiate the purchase agreement

- Assist in preparing the disclosure schedule

- Build the funds flow spreadsheet

Founder

- Review purchase agreement

- Provide information for disclosure schedule

Successful Business to Successful Exit

At Vista Point, we’ve found the optimal transaction process for maximizing valuation and optimizing key terms takes somewhere around 4-6 months. At the end of this period, the final outcome for buyers will depend on a combination of valuation price, the terms of the contract, and the goals of the founder post-transaction (such as whether they want to stay involved or walk away from the business). Regardless of your goals, an investment bank can help you move smoothly through the process and close a successful transaction.

![No deal is certain from the beginning, but [Vista Point] drew from their experience to tell us how they would engage with buyers and to explain how they expected buyers to respond.](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1342/Jonathan_Pototschnik_1_Desktop.png)

![No deal is certain from the beginning, but [Vista Point] drew from their experience to tell us how they would engage with buyers and to explain how they expected buyers to respond.](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1343/Jonathan_Pototschnik_1_Mobile.png)