Why a Competitive Process Is Important When Selling Your Business

- What running a competitive sales process looks like

- How competition between buyers improves outcomes for founders

Most founders have limited experience selling companies to maximize their outcome. So when a small pool of attractive buyers comes along making offers, the reflex reaction is to start the buying process, which is exactly what buyers want you to do.

Buyers benefit from a lack of competition in the buying process. Sellers (the founders) often shoot themselves in the foot because they don’t foster competition.

What competition in the buying process looks like

Coordinating inbound interest from buyers does not equate to a competitive process. Even if you have a relatively deep stack of indications of interest (IOIs) on your desk, there is no guarantee that the buyers who reach out are the best buyers or will even close.

A good, competitive sales process, though different for every company, involves at least the following activities:

- Engaging with many parties (more than just the buyers who reach out to you)

- Evaluating the ability of the buyers involved to "win" based on historical acquisition track record, access to financial resources, and strategic fit

- Structuring the deal process to encourage competition

- Leveraging differing valuations and term sheets to improve outcomes

- Gauging the commitment of buyers based on participation in the process and assessing the probability of close

Building a competitive process (or not building one) will affect the outcomes of your transaction in the following areas:

- Economic rewards (valuation)

- Transaction structure

- Timelines

- Closing risk

Economic Rewards With and Without Competition

The price tag on the sale of a business is one of the most visible and fought over aspects of a sale. What many founders don’t consider is that business valuations are determined the same way as the price of goods in a free market: through supply and demand.

As demand for a good increases, so does the price. In the case of business valuations, if you’re able to maximize the demand for that business, the price will correspondingly increase.

As obvious as this point about supply and demand may seem, we frequently see sellers persuaded by sly buyers to settle with an uncompetitive process where the buyer pressures the seller to:

- Work exclusively with them (often threatening to not participate if there’s any competition)

- Give them preferential treatment in the bidding/diligence process

- Sign a term sheet early with assurances that the process will be "quick and easy" (which usually turns out to not be the case)

Buyers who try to eliminate competition are looking out for their own benefit. They know that if they can remove competition they can reduce demand and thus lower the price of your business. They understand this concept because most are serial buyers—they purchase multiple companies per year and know how the process works.

You as a founder, on the other hand, will likely only go through this process a few times at most during your lifetime. If you don’t create competition in the market for your business, then you don’t maximize your economic rewards.

What can the market bear?

Buyers might suggest that the market can only bear so much in terms of price. But who are they to say? Every company is highly unique and ascribing value is difficult.

We may all have our opinions on what a company is worth, and that would obviously influence how you would interact with a buyer on a one-off negotiation. But ultimately the company is worth what a buyer is willing to pay, and there’s a good chance you’re leaving money on the table if you don’t give the "market" a chance to value the business.

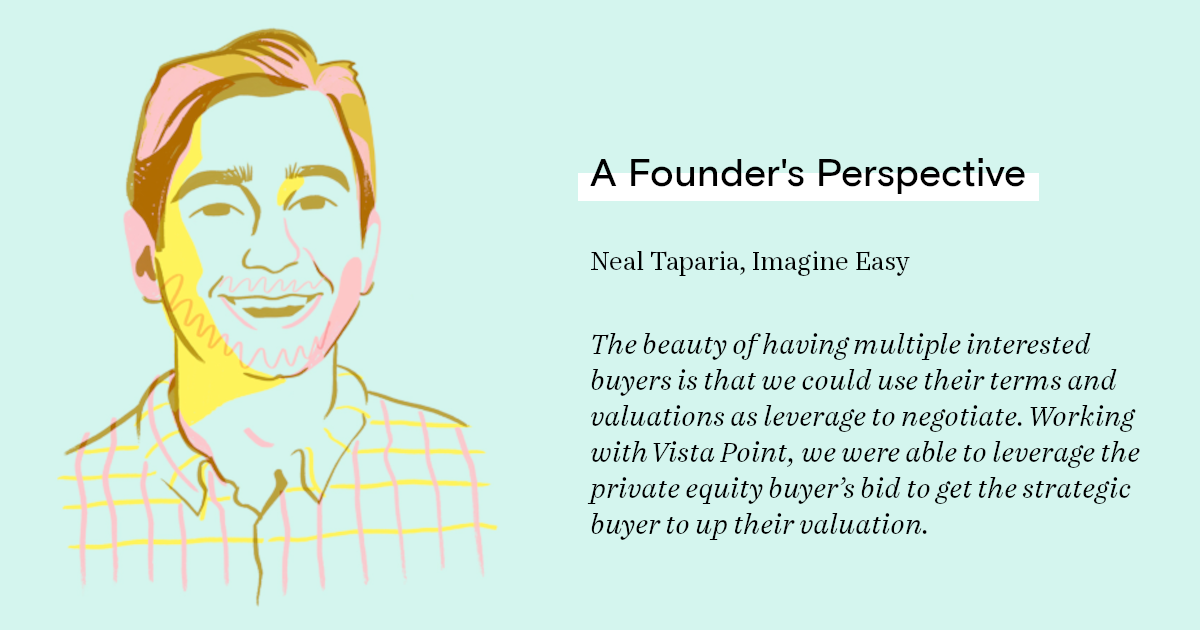

At Vista Point, we have received IOIs ranging from 2x-10x revenue for the same business based on the same data. How does a seller know if they have been speaking with the buyer who only pays 2x, especially if 99% of private deal multiples are undisclosed?

The level of competition in a process is directly connected to your economic rewards. Here is what you can expect in terms of economic rewards from a noncompetitive vs. competitive process.

Economic rewards in a noncompetitive process

When buyers know a sale process is not competitive, they are not forced to put their best offer on the table. They are incentivized to buy the business for the lowest dollar amount possible, so their valuation multiples will be low.

Of course sellers always hold the trump card as they can turn down any deal that doesn’t meet their price threshold. But leverage is limited—the best you can do is effectively pound your fist on the table and demand more money.

Fist-pounding will only get you so far. Buyers may choose to just wait you out—yours is not the only option on the table, and in a noncompetitive environment, they don’t feel much pressure to hurry. They’ll just hold off until a time in the future where they assume you will have exhausted your options and will come to terms with their "very reasonable valuation."

Economic rewards in a competitive process

What’s more persuasive than refusing a deal is telling the buyer you have other buyers that are willing to pay more, and thus their offer is simply not interesting to you.

In many competitive processes we run at Vista Point, we'll often receive 5-10 or even upwards of 35 LOIs from buyers in a competitive process. We’ve seen buyers who end up prevailing in a competitive process moving their offer up 2x or even more to prevail, which would never happen without a competitive process.

Looking deeper, of the last five software transactions we closed with revenue multiples between 5-9x, these transactions had on average 20 IOIs per transaction (ranging between 11 and 31). To further drive that point, the transaction with 31 bids priced the highest of those five deals. Competition is key to strong economic outcomes.

But valuation is not the only point of negotiation in a transaction—far from it. Transaction structure plays an important role in the outcomes for founders, in some cases taking precedence over valuation in a transaction.

Transaction Structure With and Without Competition

Buyers prefer to add some degree of "structure" to a transaction to essentially protect their investment as opposed to a clean purchase where there’s an exchange of the business for cash at close (which sellers would usually prefer).

A couple ways buyers add structure to the transaction are through:

- Deferred payments and earnouts

- Non-cash consideration

An earnout structure is when the buyer carves out a portion of the money/stock to be paid to the seller and sets objectives the seller must reach to "earn" that portion back over a set time period. The objectives are often tied back to reaching financial thresholds such as $X revenue or EBITDA in a given year/quarter.

Some of the issues with earnouts include:

Loss of decision-making power towards reaching objectives. Whether you’re selling a minority, majority, or full stake in your company, your new shareholders will have significant decision-making power in the business. As a result, they may be able to block some of the initiatives you would like to implement to reach your earnout goals.

Misalignment with buyers about performance vs. integration. After a transaction closes, buyers are going to be focused on integrating the acquisition into their existing systems. You, on the other hand, will want to close off the business to integrations/firm-wide initiatives as these will cloud the ability to measure the earnout performance and distract you from achieving the earnout.

Misalignment with buyers about the cost and value of earnout objectives. In some cases the value gained by the buyer if the earnout objective is hit might not be worth the cost in paying out the earnout, so right out of the gate you’re misaligned with buyers.

Market risk. Unexpected market shifts outside your control can inhibit your ability to reach earnout thresholds.

The earnout portion might be 10%, it might be 50%, but in our experience earnouts are extremely risky and rarely paid out. When we negotiate on behalf of our clients, we don’t consider earnouts as worth nothing, but the value is highly discounted and we negotiate heavily on this point.

Note: In software transactions, earnouts are rare and essentially unacceptable. Sophisticated buyers should know that, so if a buyer in a software transaction proposes an earnout, that’s a serious red flag.

Non-cash consideration is when a buyer exchanges their own stock or other non-cash currency for a portion of your company’s stock, instead of using cash.

Allowing for stock might be acceptable to a seller if the buying company is publicly traded, as these assets are highly liquid (unless the stock is stuck in a lock-up provision, in which case you can’t sell the stock immediately). If the company is private, on the other hand, taking stock may or may not be a form of acceptable currency, especially depending on the percent of business value transacted as stock.

Private stock presents challenges for founders because:

Private stock is highly illiquid. Just like with your business, there’s not a freely tradable market for the stock you would acquire in a stock transaction. Even worse, now you are at the mercy of the buyer in terms of the eventual liquidation, as they call all the shots for the future sale of the business.

Valuation is unknown. Buyers can play games with the "value" of the stock they are giving you. As such, you will want to tie the valuation to some form of outside independent party (i.e. a recent funding round, 409(a)).

You lose control over the future value of the private stock. Today you own all the decisions to grow the value of your business’ stock. When integrated into the larger business, you will have very little stock and decision-making power.

As with negotiating valuation, leverage is key. If one buyer is offering a relatively rigid earnout and stock purchase structure and others are not, you as the seller have the leverage you need to demand a better structure. Otherwise, you have other options you can accept.

Timelines With and Without Competition

You might assume that involving more buyers would slow down the selling process. The opposite is true. When you have multiple buyers all competing for the same asset (your business), you will have the leverage you need to incite buyers to act quickly.

How buyers try to drive the timeline and slow down the process

At first, a buyer may appear to be moving fast as they will want you to sign a letter of intent (LOI) relatively quickly.

Founders often see these LOIs as the equivalent of finalized purchase agreements, in which the buyer has agreed to the final terms for the deal. In reality, what a buyer is likely trying to do is lock you into a relationship with them that may or may not lead to a closed deal.

The signing of an LOI in a noncompetitive process usually includes a basic form letter, with little detail and thought into outlining the key terms in the purchase agreement. Signing this LOI is followed by an unnecessarily long exclusivity period (60-90+ days long), during which you’re not allowed to engage with other buyers.

Buyers will tell you the exclusivity period is necessary to justify the time and resources dedicated to conducting due diligence. In reality, they’ve achieved the convenient side-benefit of turning your business into a call option that they may or may not invest in, depending on:

What the buyer discovers during diligence. During diligence, buyers are going to dig into your company’s finances, accounting, HR, customer data, technology and more to see what they can find. For you as the seller, there is no upside to diligence, only downside. If everything checks out to the buyer’s satisfaction, they don’t pay you more, they just close the deal as planned. But if they find anything bad, the result is a renegotiation in valuation and terms.

How your business performs during the exclusivity period. Buyers will watch whether or not you meet, beat, or miss your financial projections and then decide if they want to close the transaction. The longer the buyer can conduct "diligence" on the business, the better they are able to monitor financial performance and de-risk their purchase by verifying you hit your projections.

At the end of the exclusivity period in a noncompetitive process, the buyer will come to you with their list of issues and potentially suggest a renegotiation of price and terms. They’ll propose many new legal terms and concepts not contemplated in the LOI, oftentimes at the last hour via their high-powered attorneys, resulting in a buyer-friendly purchase agreement.

How do buyers get away with this? Because by this point they’re the only game in town and they know selling the business to anyone else would be impossible.

Sellers should drive timelines and keep the process competitive

Nothing good happens for the seller once the term sheet is signed except the deal closing—so the seller wants to get from signing to close as quickly as possible. The best motivator to get buyers to accept a quick transaction process is to encourage competition.

Buyers’ biggest justification for a long process is that they want to do in-depth diligence. However, a solid indicator of a committed and interested buyer is that they are willing to accelerate diligence and gather the information they need quickly, beginning even before an exclusivity period.

By shortening the diligence process for your competitive buyer pool, you will be able to identify the buyers who are legitimately interested in your business and not just looking for a call option.

Get legal terms upfront

Because the process will be competitive with the best buyers remaining, you will have greater leverage in establishing legal terms.

At Vista Point, we ask for all important legal terms to be aired and agreed upon upfront, before we’ve chosen a party and before we’ve given a buyer exclusivity. As a result, buyers don’t try to stuff a lot of out-of-market legal terms into the purchase agreement, since they know they are competing with other buyers.

Exclusivity isn’t required

At this point, the buyer will expect an exclusivity period. Don’t assume exclusivity periods are a given. Exclusivity periods give a lot of power to buyers, so you will want to make them earn exclusivity.

At Vista Point, we aim to coordinate a short exclusivity period (15-30 days) to paper the transaction and close. Doing so means a faster time to close and lower risk for sellers because if a buyer backs out during exclusivity, the process hasn’t been so drawn out that other offers have expired. Which brings us to the final benefit of creating a competitive process: closing risk.

Closing Risk With and Without Competition

Closing risk is the concept of a buyer signing a term sheet spelling out the terms of a transaction (i.e. price, structure, exclusivity period, legal terms, etc.) and then walking away. Assessing and measuring closing risk, which is unique to each individual buyer, starts day 1 of the process and is continually updated throughout right up until decision-making time.

Closing risk is bad for sellers because sellers lose time negotiating with a buyer who leaves the seller out to dry.

One way you can minimize closing risk is by shortening the exclusivity timeline as described above. There are, however, aspects of closing risk outside of your control.

For example, a strategic buyer in exclusivity may elect to not close if:

- Their company doesn’t hit its quarterly earnings so M&A is shut down for a period

- Their company is acquired by another party so M&A is shut down for a period

Closing risk is even more pronounced for financial buyers like private equity firms. Unlike strategic buyers, financial buyers have no strategic angle (like synergies) in making the purchase—their goals are purely financial. Consequently, they have a lot more offers on the table and are even more likely to walk away from a transaction in favor of another.

If you’ve run a noncompetitive process working with a single buyer, then you’ve put all your eggs in one basket. What happens if that basket decides not to close? You’ve run out of options.

Don’t run out of options

By running a relatively short and competitive process, you will have many buyers on the table to choose from near the end. And if you make sure they’re spending time and money on diligence upfront (in the form of accountants, lawyers, tech consultants, and more), they will be even more invested in a closed transaction.

Oftentimes there will be multiple buyers with comparable valuations and terms for the transaction. While deciding between parties can be difficult, knowing that you have multiple options to choose from is comforting.

When you do decide which party to move forward with, you will have the benefit of 2nd and 3rd place bidders in your back pocket. Because you have these options, you’ll be able to:

Keep up leverage on the 1st place bidder. Having backup options enables you to keep your 1st choice honest and do exactly what they said they were going to.

Eliminate closing risk for unforeseen circumstances. If for some reason outside your control a buyer backs out, you will have several options to choose from and won’t have to restart the process.

Running a Competitive Process: A Lot of Work, a Lot of Value

We’d be the first to tell you that setting up and running a competitive process for selling your business is a lot of work. However, if you want to get a good valuation with the right transaction structure, terms, and timelines with minimal closing risk, a competitive process is essential.