Managing Your Relationship with a Strategic Buyer or Investor

- How negotiating a deal can strain relationships between founders and future partners

- How an investment banker can serve as go-between to maintain relationships

A common concern among founders exploring M&A or raising capital is how to maintain their relationships with buyers/investors.

These relationships tend to fall under two categories:

- Longstanding relationships with other founders and CEOs in their industry who are potential acquirers

- Recently developed relationships with interested investors who reached out

In the initial stages of discussing M&A or investment with buyers/investors, the conversations tend to be very high-level and focused on all good things—existing synergies, future growth opportunities, unlocking new verticals, etc.—and seem to signal smooth sailing in a future transaction.

However, as positive as your existing relationships are, they have never been tested under the strain of negotiating a sales transaction. What many founders don’t consider is that the circumstances of the relationship will change once the real negotiation begins.

Buyers and sellers have different objectives

When selling your business, your interests as a founder (the seller) are often diametrically opposed to those of a buyer or investor. While conversations up to this point have been all about how 1 + 1 = 3, now they’ve turned into a zero-sum game where each party’s priorities become clear:

- Sellers want a high valuation, ideally paid in cash, in full, at the time of sale

- Buyers want a low valuation, with a payment structure built on stock, earnouts, and escrow spread out over time and contingent upon performance

When these two parties come together to transact, difficult conversations ensue and previously strong relationships become strained.

If you feel your relationship is the exception and these uncomfortable conversations won’t happen, consider that you can’t successfully yield the best outcome for your business without being a little tough. If you’re not having difficult, uncomfortable, sometimes even heated conversations/negotiations with the buyer, then you are likely leaving money on the table and not maximizing your outcome.

You should also consider that buyers are also professionals whose job is to maximize their own outcomes. Because they’ve repeated the M&A/investment process over and over again, they know how to orient the transaction to maximize their outcomes.

Differing objectives create future challenges

All this conversation about maximizing outcomes might leave a bad taste in your mouth. You don’t want conflict, you don’t want to come across as greedy, and you especially don’t want to sour relationships—especially because you’ll likely spend time post-transaction engaging with or even working with buyers/investors, sometimes for years to come.

If you end up selling to a strategic buyer, then bitter feelings will present the following challenges:

Strained long-term partnerships. If you continue on with the buyer during a transitional period or take a position at the acquiring company, then conflict in the transaction process can make long-term partnerships uncomfortable for everyone.

Difficulty in obtaining financial consideration. You’ll likely have some sort of finances tied up in the purchasing business following the close, whether in the form of escrow, stock, or earnouts. With escrow, 5-20% of the transaction price won’t be available to you for 12-24 months, and if something goes wrong with the M&A integration, then those funds might be placed at risk. A good relationship can minimize this risk. In the case of earnouts, hitting the earnout milestones is much easier when you’re on good terms with the people running the business.

Misalignment for future product vision or employee retention/culture. If you as the leader of the company upset a future partner, that distaste may carry over to how the buyer treats your product roadmap or personnel.

If you sell to a financial buyer (i.e. a private equity firm), the challenges can be even more pronounced. Relationships with financial buyers can last 4-6 years, during which the buyers will be sitting on your board and influencing decision-making for the business. You don’t want bitter feelings in the boardroom.

Under these conditions, the prospect of selling your business may have just gone from exciting to bleak. But the transaction doesn’t have to go that way. That’s where a skilled investment banker comes in.

Investment bankers help you achieve great outcomes and still maintain relationships

As a founder, the only conversations you should be having with buyers are the positive ones—about strategy, synergies, and the go-forward vision of the company.

These positive buyer/founder conversations are important during a transaction process because they:

- Drive the deal toward the best outcome, as buyers will ascribe more value to a business that they are excited about and see you as an eager and motivated partner

- Minimize deal fatigue and keep overall morale positive (especially during the diligence stage)

To avoid polluting the air between you and buyers, you will need to rely on an investment banker to act as an intermediary and have the tough conversations. Some of those conversations include calling buyers out when they’re:

- Providing a low valuation compared to other buyers

- Proposing a structure (cash vs. stock, upfront payment vs. earnout) that is disadvantageous

- Delaying the timeline for closing a transaction

- Introducing new terms that are unfavorable

- Changing existing terms (a re-trade)

- And others

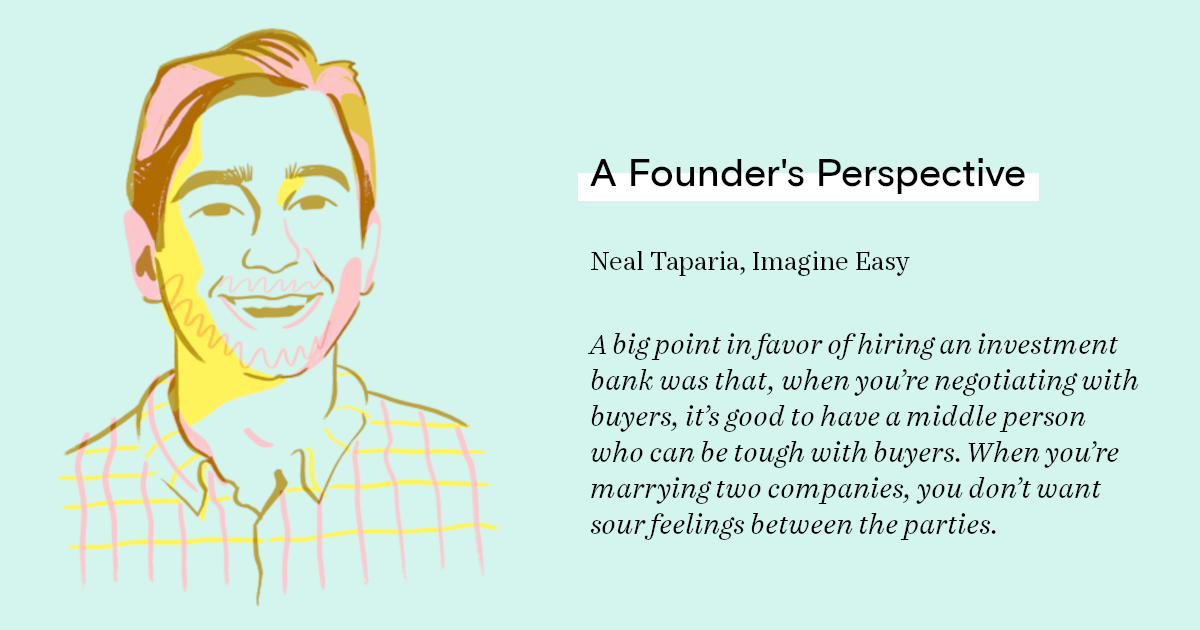

Having an investment banker be the "bad guy" can be a huge asset as it keeps buyers accountable while also preserving the founder’s relationship with the buyer. In addition, as a disinterested party with no emotional attachments to any specific buyer, an investment banker can focus on maximizing valuations and terms for founders.

What if a buyer won’t go through the transaction with an investment banker?

Founders are often concerned that hiring an investment banker will strain the rapport they’ve started building with buyers.

Buyers will stoke this fear by saying they won’t participate in a transaction if the founder hires a banker. This threat is a common scare tactic used by buyers to eliminate the involvement of an investment banker, knowing bankers will create a competitive buying process that drives valuations up and gives more favorable terms to sellers.

Almost all our clients have experienced the threat of a buyer not participating in a formal, bank-driven M&A/investment process. The truth is that those same buyers who say they won’t participate in a formal process almost always do. If they don’t, their valuation was probably so low they knew there was no chance of prevailing unless they could circumvent a competitive process.

Consider this: if a buyer sees the synergies in a transaction and values your business appropriately, why would they be concerned about you working with an investment banker?

Bankers can help you attract the best buyers

In many cases, sophisticated and experienced buyers (who tend to pay premium valuations) will consider a bank-driven process as positive, as this action signals serious intent on the part of the company pursuing a transaction.

Especially in situations where a company doesn’t have a formal or sophisticated board, hiring a banker helps buyers see that founders (sellers) aren’t kicking tires or just having M&A conversations to run a market check.

Competition creates urgency for sophisticated buyers

Running a formal, banker-led process creates an urgency for buyers to act and to lead with their best offer. When you hire an investment banker to create a competitive process, you send the message to buyers/investors that if they don’t acquire or invest in your business then another will, and that other buyer/investor will either turn your company into a strong competitor or into a more expensive acquisition later on.

Close your transaction on good terms with the buyer

If you don’t involve an investment banker in the transaction process, then you’re left with the dilemma of whether to burn bridges now for a better outcome or sacrifice the outcome for the sake of good relationships going forward with a valued partner. Neither option is ideal, and you shouldn’t have to choose between them.

If done correctly, investment bankers can shoulder the responsibility of hard conversations so that when the transaction is over and done, neither side of the table is shouldering resentment.