Why Framing Your Business Matters When Preparing to Sell

- What framing means in the context of selling your business

- How to avoid the risk of over- or under-framing

- How to appropriately frame key aspects of the business

The first impression you make when presenting your business to buyers and investors has a significant effect on the final outcome of a transaction.

You only get one chance to make that first impression. As such, you’ll want to make sure you properly frame your business for buyers and investors. Otherwise, they may misinterpret key aspects of your business, leading to a suboptimal outcome.

What Is Framing?

As founders, you have a deep understanding of the nuances of your company and industry. This knowledge serves as a lens through which you interpret your business metrics and KPIs.

Buyers and investors don’t have the benefit of this same information or experience. Instead, they have specific metrics they’re interested in, along with performance benchmarks/standards they expect for each metric. At face value, your company’s metrics may not meet their standards, which will negatively affect interest in the deal or your valuation.

Framing helps bridge the gap between the two perspectives by presenting underlying company data and trends that might not be plainly obvious in surface level metrics.

Tell the complete story

Consider the following example: you run a SaaS business that accepts customers of all contract sizes. As a result, you have a large cohort of relatively low-revenue customers who self-service but also churn at a high rate. These customers only represent 5% of your revenue, but because they’re a relatively large cohort in terms of customer count, they’re driving down your customer/logo retention rate.

At face value, buyers and investors (referred to as buyers from here on out) will look at your retention rate and express concern, which will be reflected in their valuation of your company. Buyers aren’t seeing the full story, which is where framing comes in.

In this case, framing your business would involve separating out the low-value customers so you can show buyers your high retention rates for the high-value customers, casting a positive light on your business.

Avoid the risk of under-framing or over-framing

Framing a business occurs on a spectrum.

At one end of the spectrum, you could under-frame and provide raw P&L or customer data to buyers without any framing, relying on the buyer to come to their own conclusions. Under-framing creates misconceptions about the business and leads buyers to lose interest or give a low valuation.

On the other end of the spectrum, you could over-frame and try to explain every aspect of the business and why it’s the "best-in-class," "revolutionary" or the "Uber of X." Over-framing often involves trying to cloud weaknesses of the business through creative manipulation of information, which breeds distrust among buyers.

Neither extreme is ideal—you want to strike a balance between the two.

How do you know when and what to frame?

In order to properly frame your business, you’ll need to know what information buyers want to see and what their benchmarks/performance standards will be. This information will vary from industry to industry—for example, buyers will expect different information/performance standards for B2B enterprise software vs. SMB internet platforms.

Many founders rely on investment bankers to help with framing. Investment bankers are experts at telling the complete story of the business to help founders realize a better outcome.

Our bankers at Vista Point focus their framing around 6 core areas:

- Financials & Customer Data

- Growth Opportunities

- Technology & Product

- Personnel & Founder Involvement

- Company Weaknesses

- Total Addressable Market (TAM)

Framing Business Financials & Customer Data

Framing the financials and customer data of a business involves taking a deep dive into the trends and dynamics of the corresponding metrics, such as:

- Revenue

- Gross margin

- Sales

- Marketing efficiency (LTV, CAC, payback periods, ROI, etc.)

- Retention rates (net, gross, logo)

- ROI for customers from using your product

- Repeat purchase trends/growing share of budget

- User adoption and usage rates

When an investment banker calculates and frames these metrics, they make sure to go back to the underlying raw data source so that the metric holds up during the due diligence phase.

At Vista Point, we focus a lot of time on framing revenue, as revenue is one of the most high-profile metrics buyers evaluate, especially in recurring revenue business models like enterprise SaaS. Specifically, when framing revenue we emphasize strengths of the composition by showing there is:

Little to no concentration of revenue. Buyers like to see that your company doesn’t rely on a small group of customers to provide a large percentage of revenue.

A large percentage of revenue that is recurring or reoccurring. Especially in SaaS, buyers like to see that a large portion of revenue is contractually repeated (recurring revenue). In some cases for internet businesses, we can frame revenue as reocurring and achieve similar outcomes as for recurring revenue even if the revenue doesn’t contractually recur.

High net, gross, and logo retention rates. These metrics indicate how well you keep your customers at the same or greater level of revenue. At Vista Point, we’ll evaluate the best frame of customers for these retention rates based on dimensions like length of time using the product, spending over a certain threshold, and others.

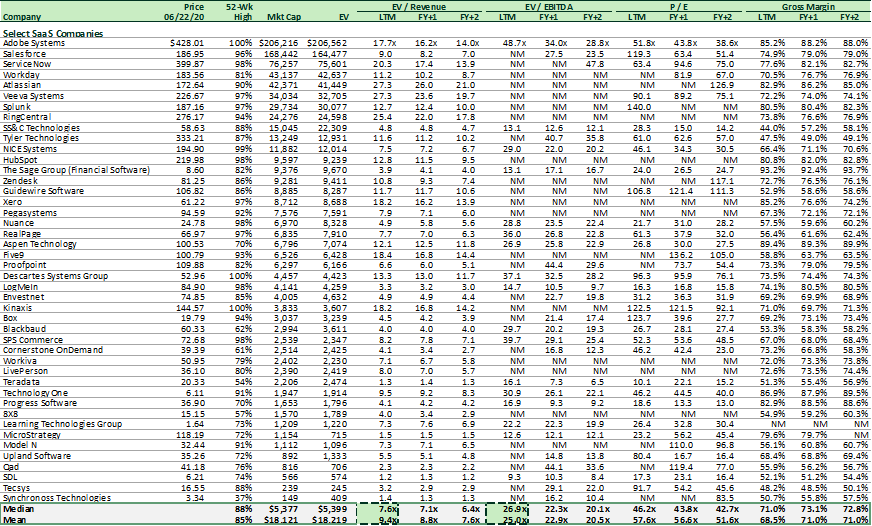

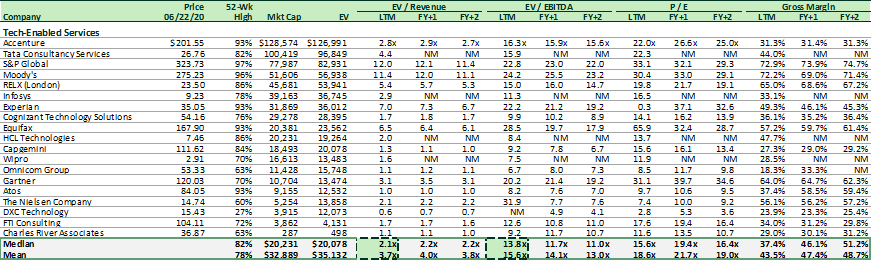

How you position retention can dramatically affect valuation. Consider the difference in valuation multiples of revenue between SaaS businesses with high retention and tech-enabled services businesses with lower retention. For the below SaaS companies we analyzed, their valuation multiples (enterprise value / revenue) sat at a median of 7.6x and mean of 9.4x. Compare those multiples to those of tech-enabled service businesses, at a median of 2.1x and mean of 3.7x.

Valuations on SaaS Businesses

The companies included in the below analysis are considered industry leaders in the SaaS sector and therefore representative of top valuations in that sector.

Valuations on Tech-Enabled Services Businesses

The companies included in the below analysis are considered industry leaders in the tech-enabled services sector and therefore representative of top valuations in that sector.

If you can successfully and truthfully identify the correct customer frame to show buyers that revenue is highly recurring and not concentrated, you can expect a higher valuation multiple. Similar logic applies to other financial and customer data metrics.

Framing Growth Opportunities

Buyers are interested in companies that are great today and even better in the future. As such, showing buyers that the business is proactively thinking about growth for the future is critical.

When framing growth opportunities, your investment banker will focus on:

Demonstrating how these opportunities yield short, medium, and long-term benefit and the associated risk of each. Your banker will show buyers how your company has both immediate, low-risk opportunities to capitalize on as well as larger, riskier opportunities to pursue in the long-term.

Highlighting a product roadmap that feeds directly into growth opportunities. Such a roadmap might include details about how to penetrate new customer end verticals or use a channel partner to get broader product distribution.

Fleshing out how today’s internal investments will contribute growth in the future. For example, you might describe how you’re currently enhancing your customer success team to improve your net retention rate (which represents growth via renewals or upsells within your existing customer base).

Identifying aspects of the business where limited capital has historically limited growth. Minimally funded, founder-led companies often have known growth opportunities that have remained on hold due to a lack of capital (marketing hires being a great example). In these cases, a banker can easily characterize these aspects of the business as low-hanging fruit in terms of growth.

Buyers pay a premium for immediate growth, and that premium is secured with the promise of future growth.

Framing Technology & Product

When framing your company’s core technologies/products, buyers are primarily interested in three key questions:

How is your technology/product differentiated? Related to the concept of defensibility, buyers are interested in knowing how your widget is different from any other widget in the market. Does it require less onboarding? Is it self-service? Do you need less resources to market it? Any form of differentiation is favorable to buyers.

Is your technology/product position defensible? The last thing a buyer wants is to purchase a company only to find that the product is easy to replicate or disrupt. When framing your product, you will want to demonstrate how your position is defensible, either because you have patents, trade secrets, key supplier/OEM agreements, a headstart on the competition, or other advantages over competition.

Which is better: building the technology myself or buying your company that already built it? Build or buy is a classic question for strategic buyers. Your banker will help you show the total investment (in terms of time and dollars) to develop your technology. The primary goal in doing so is to show that creating the product would take longer than expected and, especially where speed-to-market is important, the M&A option would be more effective.

Framing Personnel & Founder Involvement

No business exists independent of its personnel, so buyers are justifiably concerned with the roles and involvement of various personnel, especially the founders. The main interest in personnel is a focus on succession—will the management team be able to run the company following the transaction?

Some tactics your investment banker will use to frame personnel include:

- Highlighting the backgrounds and achievements of the management team

- Discussing how new capital/partnerships could fill gaps in management

- Showing how second layer management is capable of or already running day-to-day operations

- Allowing buyers to interface directly with key contributors in the company

- Outlining equity compensation for key employees going forward (to show commitment)

- Removing founders from certain diligence discussions so buyers get used to going to someone other than founders for information

The question of succession is particularly pertinent if the founder intends to leave post-transaction. As such, part of framing the business is highlighting that the founder is not critical to day-to-day operations, which can be tough for founders. However, focusing on the contributions of other people in the organization will make it easier for founders to justify limited involvement after the deal closes.

Framing Company Weaknesses

Each business will have a unique challenge or characteristic that buyers and investors need to understand. In addition, there will be developments during the transaction process that need proper framing. In order to mitigate the risk of deals falling through later in the process due to weaknesses, you will need to explore company weaknesses as soon as reasonably possible.

Common weaknesses to address include:

- Pending lawsuits

- Declining growth

- A highly concentrated customer base

- A low margin profile

- Declining annual contract value (ACV)

- Turbulence in the end market

The key to framing weaknesses is to demonstrate that these weaknesses are not relevant when valuing the business or are an opportunity for the buyer to improve on post-transaction.

A good investment banker will work hand in hand with the client in order to help establish the appropriate frame. One common tactic is to chalk the weakness up to a lack of capital (which is why the founder is having the conversation with buyers/investors), but there are other tactics as well.

Framing Total Addressable Market (TAM)

One question buyers/investors will always bring up (especially private equity investors) is "What’s the TAM?" Since buyers are hoping to yield a return on their investment, they want to verify two things about your market:

- Your market is big.

- Your market is growing.

One way to maximize TAM is to consider other verticals you don’t currently serve but could in the future. Buyers will look favorably on companies looking to grow their TAM by addressing new markets.

Founders are particularly vulnerable to over-framing when calculating TAM, as they often use the total revenue or income of their target customers as the size of their total market. This approach is flawed because not all revenue or income is available for spending on a company’s specific product.

For example, if you run a B2B software company, a more accurate way to calculate TAM would be to consider the size of company budgets allocated to spending on software. Your investment banker can help you determine what is the best way to limit TAM while also maximizing its size.

Frame Well, Sell Well

Like a job candidate putting forth a resume, framing is about putting your best foot forward to make a good first impression. If you don’t take the time to frame, then you’re behind in comparison to other companies pitching to the same buyers for limited resources.

There’s a right way and a wrong way to frame. If you want to get it right the first (and only) time, then your best bet is to hire an investment banker who has the experience to help cast your company in the best light possible.