The Entrepreneur’s Dilemma: Selling an EdTech Business During a Growth Phase

- Why you should sell when you're winning

- How buyers reward growth

- The importance of liquidity as a founder

Over the course of the last 5 to 10 to 15 years, you’ve built an EdTech company that’s growing in value at a rate to dwarf the market—something most entrepreneurs only dream of.

In your current situation, you might come to the conclusion that you should ride the wave as long as possible, growing the value of your company and your equity along with it. Once growth plateaus, then you should sell, right?

Not right.

Waiting for company growth to plateau (or expecting to predict an upcoming plateau and sell the company before then) is not a good exit strategy. Here’s why.

The Dilemma: Why Sell When I’m Winning?

As we at Vista Point advise high-growth EdTech companies about the right time to sell, we often get the question, "Why would I sell when I’m growing 30% YoY? Where else can I get that type of return?"

The question is valid and the logic seems sound, because when you grow your business 30% each year, then you’re likely increasing the value of your equity at roughly the same rate, which is a lot of value creation.

But consider the following:

You have a highly concentrated financial risk in a single asset

Having all your assets tied up in a highly valuable company is a high-class problem, one many people wish they had.

But there’s a reason private equity firms, venture capital firms, financial planners, and wealth management professionals don’t put all their eggs in one basket but instead spread their assets across multiple investments: If something goes wrong with one investment, they don’t want to lose their shirts.

You may feel equipped to manage the challenges your EdTech business may face in the future. After all, no one understands the state of the company better than you after pouring your blood, sweat, and tears into it over the last batch of years. But even you can’t fully predict the future of your company. If the company experiences challenges, your only asset is at stake.

To be frank, the current market for EdTech is very challenging. COVID created a surge in demand, but those investments are starting to melt away. That said, many of the dollars allocated for EdTech spend are still yet to be used. With the fiscal cliff looming, edtech companies will likely see an increase in demand.

Still, the question is whether retention rates will hold strong when funding is discontinued. The market is much more complex than it was 2 years ago and being able to properly position that to the market is growing increasingly difficult.

Your attitude will change with time

When you first started, you probably took some pretty huge risks to get to where you are today. But now that all your personal wealth is tied up in a high-value business, taking huge risks and betting the farm on big moves doesn’t seem as exciting.

Instead of seeking out risk, you’ll probably start doing your best to avoid it. You might find yourself thinking more about protecting a business that is clearly valuable and the sale of which represents life-changing amounts of money.

You can’t predict plateaus

A common fallacy entrepreneur’s fall into is the idea of being able to predict and sell before a plateau in growth or an economic downturn.

While entrepreneurs are good at being optimistic, they are by no means clairvoyant. Founders might be fooling themselves if they think they can see a plateau coming.

Plateaus are impossible to predict because changes in business performance can come from various forces, including forces that are completely outside of your control. Consider what happened to the value of companies and the economy when:

- The 9/11 attack happened

- The 2008 housing market fell, leading to worldwide recession

- Web users began migrating from desktop to mobile

- COVID-19 caused demand for EdTech to skyrocket initially, but then slowed considerably

The above examples only illustrate extreme, worldwide market movements—they don’t take into account the thousands of industry specific changes in the EdTech market like the emergence of unforeseen competitors, changing regulatory conditions, or evolving customer preferences. When an unexpected plateau hits, you’re going to leave a lot of money on the table because informed buyers don’t pay premiums for plateaus.

The current state of the EdTech market is evening out now that the explosive new investments and budgets allocated during a world-wide pandemic are starting to melt away.

As the tailwinds from the pandemic slow, there is greater focus on admin software, which tends to have more defined budgets and mission critical assets. For higher education, admission rates still seem to be falling and finding a bottom to that is going to be important for student related solutions. Similarly, admin software will still hold strong as universities look to become more efficient and more attractive to students. At the same time, universities are not as reliant on government subsidies, which means they have a greater stickiness on their budget and are not seeing as much impact as K-12.

The market is much more complex than it was 2 years ago, and EdTech founders need to think through how they maintain some of the growth as properly positioning an EdTech software is growing increasingly difficult and the marketing is leveling out.

Buyers Reward Growth, Not Plateaus

In any transaction, buyers are trying to answer the following questions:

- Why are you selling your business now?

- What do you know as a founder that I don’t?

Strategic buyers and private equity firms in the EdTech space are going to do their homework. They’re going to pick up on any whiff of impending growth slowdowns or growth challenges.

As a result, you should sell into growth. Founders will experience a HUGE difference in valuation when selling into strength vs. selling into a plateau. If you wait for a negative outcome like a plateau or downturn to trigger your sell reflexes, you’ll be in a weaker position relative to buyers and will lose out on what’s known as the multiplier effect.

The Multiplier Effect: What Really Drives a High Valuation

As you’re well aware, the value of your company isn’t just based on revenue or profitability for the current time period, but on expected value generated over time. Most often, a valuation is estimated based on a multiple of revenue.

Why is this important? If you can identify ways to improve the multiple, then you increase the perceived value of your EdTech company for buyers.

Two primary factors are growth and revenue milestones.

Multiples from growth

Growth businesses sell for significantly larger multiples than non-growth businesses, and the higher the growth, generally the higher the multiple.

To answer founders’ primary concern of why sell when they’re winning, the reason is you want to take advantage of the success and strength in the business and capitalize on this as a growth multiple for the valuation.

As a contrived example, a company with revenue of $10M per year and growing at 30% might have a multiple of 5x, so it would be worth $50M today. On the flip side, a company with revenue of $20M per year but only growing at 10% per year might have a 2.5x multiple, worth also $50M, but it likely took another 4-6+ years to reach that point.

If you wait for growth to slow, then:

- You take on the additional business risk of change in your business, industry, or market.

- You could miss out on higher multiples at current growth rates.

Multiples from revenue milestones

As companies pass certain revenue milestones, their valuations tend to make a jump. At Vista Point, we tend to see step functions on valuation at $10M and $25M ARR for SaaS businesses.

Buyers pay attention to these milestones—if you hit a milestone recently, you probably started receiving calls from interested buyers. Their interest in your company will manifest itself in the multiple they use to value your business.

![When we hit $10M in sales, we had a turning point where we thought, “Okay, we need to do something.” We were still growing at 30% year-over-year, but we didn’t have the resources to serve [other] disciplines... The general preference among the board mem](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1289/Smita_Bakshi__Desktop_.png)

![When we hit $10M in sales, we had a turning point where we thought, “Okay, we need to do something.” We were still growing at 30% year-over-year, but we didn’t have the resources to serve [other] disciplines... The general preference among the board mem](https://cms.vistapointadvisors.com/system/uploads/fae/image/asset/1290/Smita_Bakshi__Mobile_.png)

Which Is Worse: Selling Early or Selling Late?

As we’ve already acknowledged, timing a sale at an exact peak is impossible. By the time you recognize a peak, you’ll end up selling late at a lower multiple.

But if you sell too early, even at a high multiple, couldn’t you end up leaving a lot of money on the table? Yes, that’s the trade-off. But here are some important points to consider.

If you sell early, you do take a potentially large sum of money off the table. But, you also have ways to structure your finances to capture additional upside. For example, you could:

- Sell only a portion of the business instead of the whole and stay involved, or

- You could keep some equity riding in the business whether you’re involved or not to take advantage of upside.

If you sell late, well, that’s tough. You had an asset worth a lot of money months or years ago, and now it’s not. All the while you’ve spent time focusing on the business when you could have been starting a new business or doing something else with your time. This regret is painful, and can lead to bitterness.

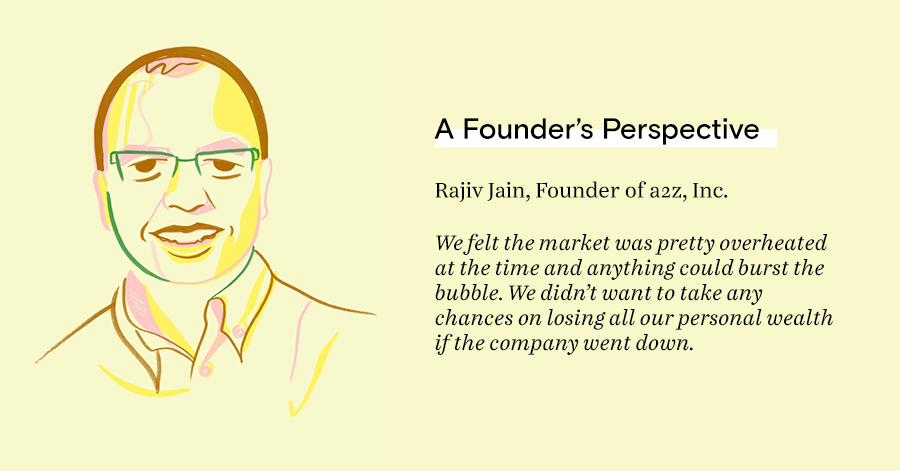

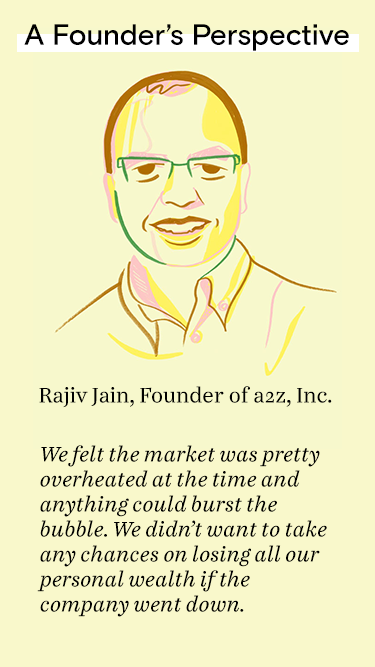

Selling Early Enables Diversification and Liquidity

Timing does play a role in selling your business, but the primary goal is to diversify your assets and improve liquidity so you don’t lose your shirt.

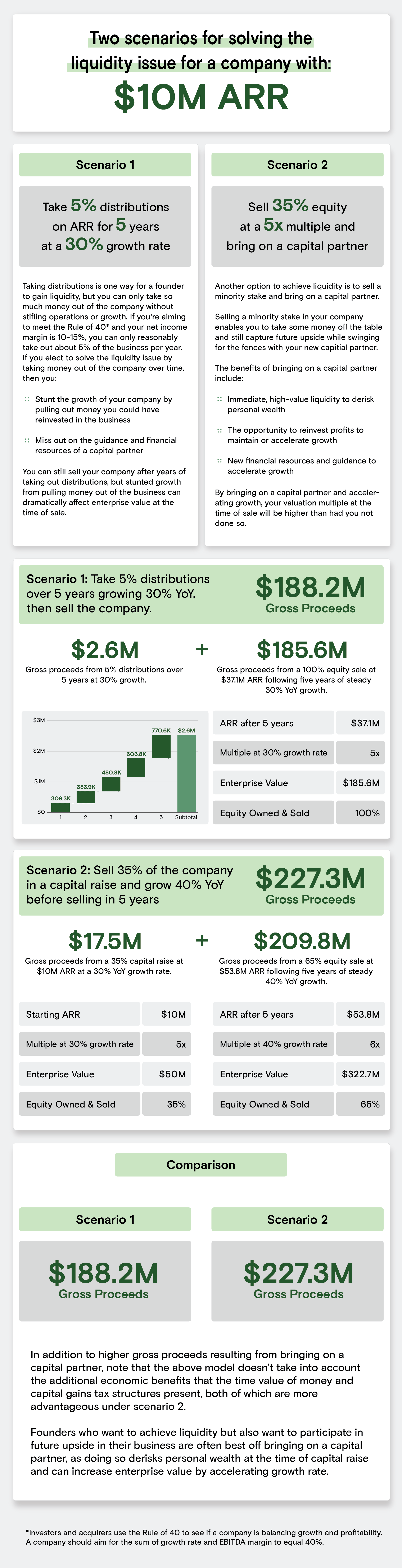

There are several solutions to the liquidity problem, some better than others.

One solution: Take out cash from the business

Some founders will try to solve the liquidity issue on their personal balance sheet by taking cash distributions out of the business during times of profitability. However, this might not be the best long-term tactic for improving the enterprise value of the business.

For instance, if you take away cash-flow that could have been directed to revenue-generating initiatives, you’ve hurt the equity value of the business. The decrease in value isn’t dollar-for-dollar the amount you took out of the business, but much higher due to the multiplier effect.

In addition, you also might change the valuation paradigm, causing buyers to value your business as a multiple of EBITDA instead of revenue, which will significantly hurt the long-term equity value of the business.

On top of all that, if you take out dividends/distributions, you’ll be taxed at the personal income tax rate on that income, as opposed to putting the money back into the business and pulling it out with more favorable tax structuring during a sale of the business.

A better solution: Bring on a capital partner

Instead of stunting the growth (and value) of your business by taking out cash distributions, bringing on a capital partner can help you achieve liquidity while also maximizing your outcome.

When you sell your business, you’re not restricted to a full-sale. You have several options for the transaction, depending on your financial goals and your goals for the business. A few include:

- A minority sale, which allows you to cash out on a portion of the business but maintain strategic control

- A majority sale, which still gives you some upside in the future of the business but gives you liquidity on the majority of your ownership

- A full sale, which gives you full liquidity to do as you wish

The below infographic demonstrates how bringing on a capital partner is better in the long term for gross proceeds to the founder.

More Reasons to Sell Other Than Liquidity

Liquidity is a primary goal of many of our clients, but each founder has their own reasons for selling. Some common reasons we hear include:

- Not wanting to deal with the HR issues that crop up daily and require attention

- Not having the skill set to drive the company forward at scale

- Not wanting to be involved in the transition from a product-first business to a marketing and sales-driven business

- Having family challenges that need to be addressed

- Wanting to move onto something new

Regardless of your reasons, an eventual sell is in your best interest. Making the paradigm shift to selling into a growth phase can be difficult, but the ultimate outcome is well worth it.