2021 State of the U.S. Mortgage Software Market

- How housing market demand is driving digitization in loan origination

- Why fragmentation in mortgage software will lead to consolidation

- What high stock prices and private equity dry powder mean for M&A in mortgage software

In consequence of a surge in housing demand in the past year, the mortgage software market has seen impressive growth. As such, companies in the space are well-positioned to pursue an M&A or capital raise transaction in the near future.

In addition to favorable market dynamics leading to all-time highs in mortgage applications and refinancing, other factors making 2021 and 2022 optimal times to pursue a deal include:

- A strengthening focus on digitizing the loan origination process

- Fragmentation in the mortgage software space creating an opportunity for consolidation

- High stock values and an excess of private equity dry powder to be placed

Below are details on these key trends affecting M&A prospects in the mortgage software space.

Favorable Market Dynamics Leading to High Lending Volume

The circumstances of the COVID-19 pandemic created ideal market conditions for a surge in home buying. At a macroeconomic scale, all-time lows in interest rates made monthly mortgage payments more affordable. At a microeconomic scale, stimulus payments and other benefits resulted in American households having the highest savings balance ever, easing the burden of a down payment.

The result was a dramatic spike in home sales. Specifically, in the second half of 2020, roughly 5.5 million homes sold, compared to only 3.7 million sales in the first six months of 2020.

More moves meant more mortgages, and together with low interest rates fueling a mass of refinancings, the highly cyclical mortgage market is at a historic high. From 2019 to 2020, total mortgage origination value increased 74% from a pre-pandemic H2 2019 ($1.15T) to over $2T in H2 2020 (including new mortgages and refinancing).

Of course, the cyclical housing market is likely to see a drop in demand in the next few years as work-from-home culture settles in. Still, due to the pandemic, a decade of technological adoption and implementation happened in just a matter of nine months, expediting product adoption and growth in the space.

Even in a post-COVID world, the developments in digital lending—from simple information updates to complete end-to-end mortgage origination—will continue to proliferate as consumers opt to handle their mortgage needs online vs. in-person.

Digitization Is Fueling Mortgage Software Market Growth

Given that mortgage providers consider time to close as their number one KPI, lenders have adopted software at high rates to create efficiencies in the process. Software providers who streamline the application and loan origination processes are seeing the benefits of this trend.

Among the most prominent technology investments mortgage players have made is in the mortgage application experience (or point of sale/POS). Customer-facing technology has become a critical value point in the mortgage origination process, as evidenced by Quicken Loans’ reported investment of ~$400M in its front-end.

Of course, the application experience is just one aspect of the loan origination process among many. As different pain points emerged across the loan lifecycle, best-in-class point solutions have correspondingly emerged. The result has been rapid development in the areas of computation, mortgage origination, and information verification solutions, creating fragmentation in the mortgage technology market.

Consolidation in the Mortgage Software Space Is on the Horizon

The disparate nature of point solutions has created an untenable number of APIs, signaling a need for the market to be consolidated under one tech stack. Data integration across the entire process is causing vendors to look to consolidate their solutions, maximize speed, profitability, and end customer value.

In other words, the biggest players in the mortgage space will look to acquire smaller players to capture as much share as possible of the standard ~$400 processing fee of a mortgage application.

The biggest targets for consolidation will be the systems that either provide the application process for clients or store and process mortgage data in their data warehouses and computational engines. These systems have a captive audience to sell additional solutions to, making them the most desirable candidates for acquisition.

But the market opportunity for key players isn’t limited to claiming wallet share within a saturated market. While the rise of digital lenders has been nothing short of meteoric, larger, "blue-chip" lenders have been slower to adopt necessary software.

These blue-chip lenders represent a massive market opportunity. Software providers who can successfully service the end-to-end application and origination process (potentially via consolidation) will be better positioned to serve the largest lenders.

M&A Activity Made a Full Recovery in the H2 2020

Along with the pressures for consolidation in the mortgage software space, the way in which M&A activity made a full recovery in the second half of 2020 and early 2021 further signal that now is an ideal time to pursue a transaction.

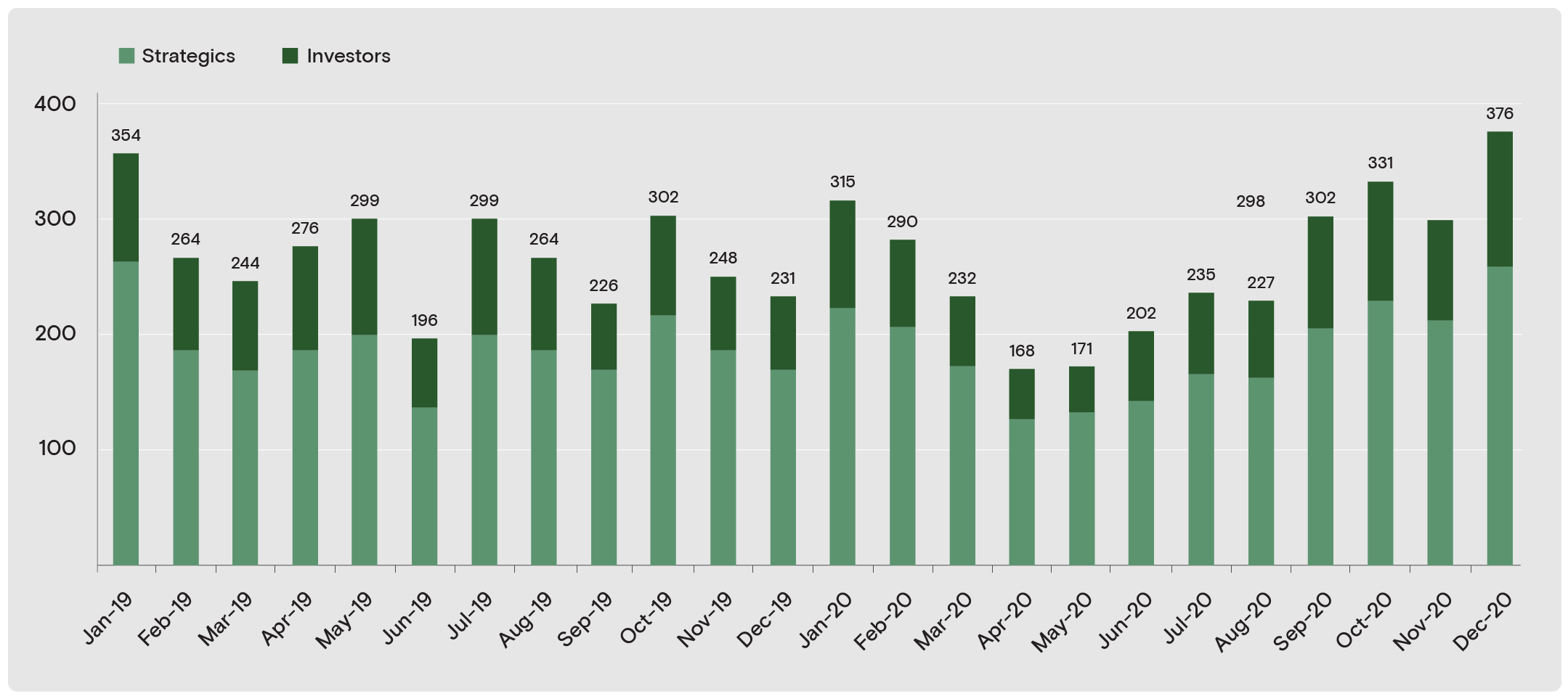

Matching with our expectations, the back half of 2020 saw a V-shaped recovery for valuations and M&A following the initial COVID-19 shutdown (see the figure below).

Technology M&A Transactions by Month by Investor Type

Technology M&A fell in the early months of the pandemic, but rebounded with a vengeance.

Q1 2021 continued to rebound, posting YoY growth of more than 17% in M&A activity compared to a pre-COVID economic climate. In other words, M&A activity is growing over the previous baseline, not just coming out of the pandemic-induced trough.

The quick rebound in M&A activity comes as the result of:

- A large rise in stock prices, which strategic buyers have used as fodder for acquisitions

- A huge amount of dry powder that private equity firms held during H1 2020 and are now looking to place

This growth in M&A activity signals not only a return to normal M&A levels, but rather continued, explosive growth due to the ever-expanding levels of private equity dry powder and the proliferation of high-quality assets.

A Path to Exit for Mortgage Software Founders

For mortgage software providers looking to pursue an M&A transaction in the near future, the window has never been better for an exit.

In light of rapid technology adoption and a large growth opportunity to serve blue-chip lenders, large strategic players and private equity firms equipped with valuable equity and excess dry powder will be looking to consolidate within the fragmented mortgage software space.

Founders who recognize and capitalize on these conditions are in a great position to pursue an M&A or capital raise transaction in 2021 or 2022.

Vista Point Advisors is a boutique investment bank that focuses on advising founder-led companies in the Software and Internet industries. We focus exclusively on sell-side M&A and capital raising transactions.

Learn more about our team or see our recent transactions.