SaaS, GAAP Revenue, and M&A: What Founders Need to Know

- How buyers interpret revenue as part of the M&A process

- Why private SaaS founders need to recognize revenue according to GAAP before engaging with buyers

- An introduction to ASC 606, the GAAP standard for recognizing revenue

Because private companies are not subject to the same financial requirements as publicly traded companies, founders of private SaaS companies often forgo implementing generally accepted accounting practices (GAAP) to avoid the resource cost.

However, as a SaaS founder, if you’re contemplating M&A (i.e. bringing on a strategic partner, selling the business outright, or financing through private equity), you will need to be in compliance with the basics of GAAP—namely revenue recognition.

Why GAAP Revenue Recognition Is Important for Private SaaS

Revenue recognition is a staple of GAAP and accrual accounting.

Accrual accounting, in a nutshell, recognizes revenue at the time revenue is earned, as opposed to cash accounting, where revenue is recognized when cash changes hands from customer to SaaS provider.

Using the SaaS model as an example, under the accrual accounting methodology, the paid-in-full booking value of a multi-year SaaS contract would not be recognized at the time the payment is received, but instead amortized (spread out) over the length of the contract.

While cash accounting may be operationally easier to manage, accrual accounting paints a more accurate picture of the financial health of an organization, for several reasons:

- Revenue is recognized at the same time as the costs incurred to generate that revenue, giving a clearer picture of profitability.

- Cash revenue that has been received for services yet to be provided places a liability on a company, which isn’t obvious under cash accounting.

- Customer health and related revenue churn are easier to track with accrual accounting, better equipping you to improve retention rates.

How investors interpret SaaS revenue and the importance of properly recognizing revenue

While private SaaS companies may not be required by law to implement GAAP-compliant revenue recognition, doing so is in their best interest if looking to pursue a transaction, for the following reasons:

- Potential investors or acquirers want the cleanest lens to both (a) interpret how a SaaS company earns revenue over time and (b) compare to portfolio companies and other prospective investment opportunities.

- SaaS revenue that has been properly amortized appears less volatile from month to month, granting the impression of predictability for which buyers will pay premiums.

- Gross and net revenue retention rates, key diligence points in a transaction process, will be highly volatile if cash accounting is used as the basis for analysis.

- Profitability margins calculated on a cash basis can be skewed positively when cash is collected and negatively when sales/renewals are not made.

- If revenue is not properly recognized, you will have a limited basis for negotiation when it comes to working capital adjustments at deal close, which could lower the final purchase price of a deal without a clear sense of what it will cost to service the revenue that’s yet to be earned.

Buyers will expect revenue and associated metrics to be calculated according to principles of accrual accounting. As a founder, presenting a P&L based on cash accounting may result in buyers telling you to come back with properly recognized revenue. At worst, buyers will find out on their own during diligence that revenue was not properly recognized, which will result in a violent retrade or a broken deal.

In other words, instead of paying premiums for highly predictable SaaS revenue, buyers will treat revenue as transactional and valuation will accordingly take a serious hit, or a deal will not materialize at all.

Given the implications for M&A, founders should reevaluate implementing GAAP-compliant revenue recognition based on the industry standard known as ASC 606.

GAAP-based revenue recognition: ASC 606

ASC 606 (or IFRS 15 in Canada) is a standardized process for recognizing revenue, encapsulated in the following steps:

- Identify the contract with a customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price (across time)

- Recognize revenue when or as the entity satisfies a performance obligation

For a SaaS company, this process could look something like the following:

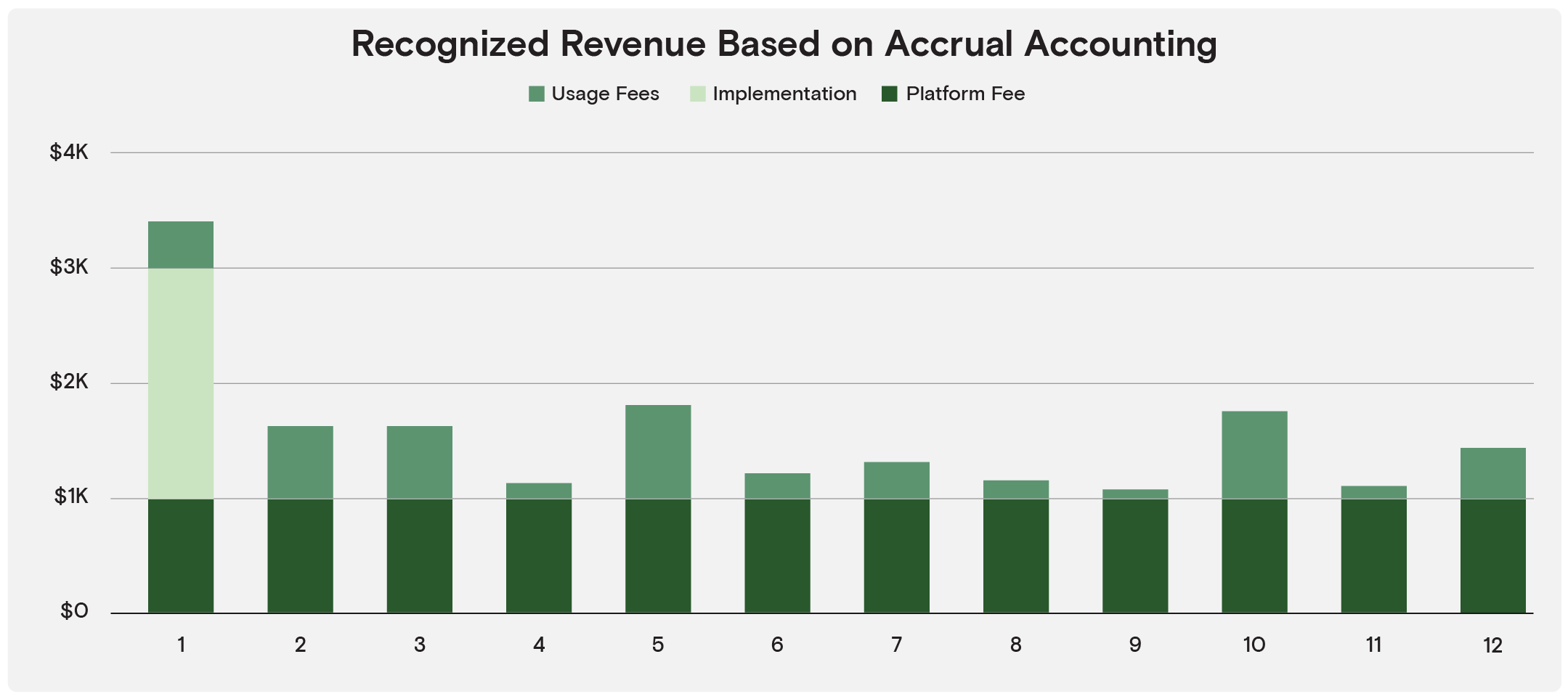

Consider a SaaS company that sells an $18,000 contract with a 1-year term. Included in that contract is the platform fee ($12,000) and an implementation fee ($2,000), both paid in full at the beginning of the contract (m1). In addition, the contract includes usage fees, which will be incurred irregularly throughout the term of the contract.

While the full booking value of this contract is paid in full at m1, the revenue won’t be fully earned until completion of the contract. As such, the revenue from the platform and implementation fees would only be recognized as they’re earned (usually monthly). Any usage-based fees would be transactional, and therefore recognized in the period in which the usage revenue was earned as well.

The below chart shows how revenue would be recognized across the length of the contract. Note how the platform fee is spread across the term of the contract, at the time in which the revenue is earned for those services, not when the cash enters the business.

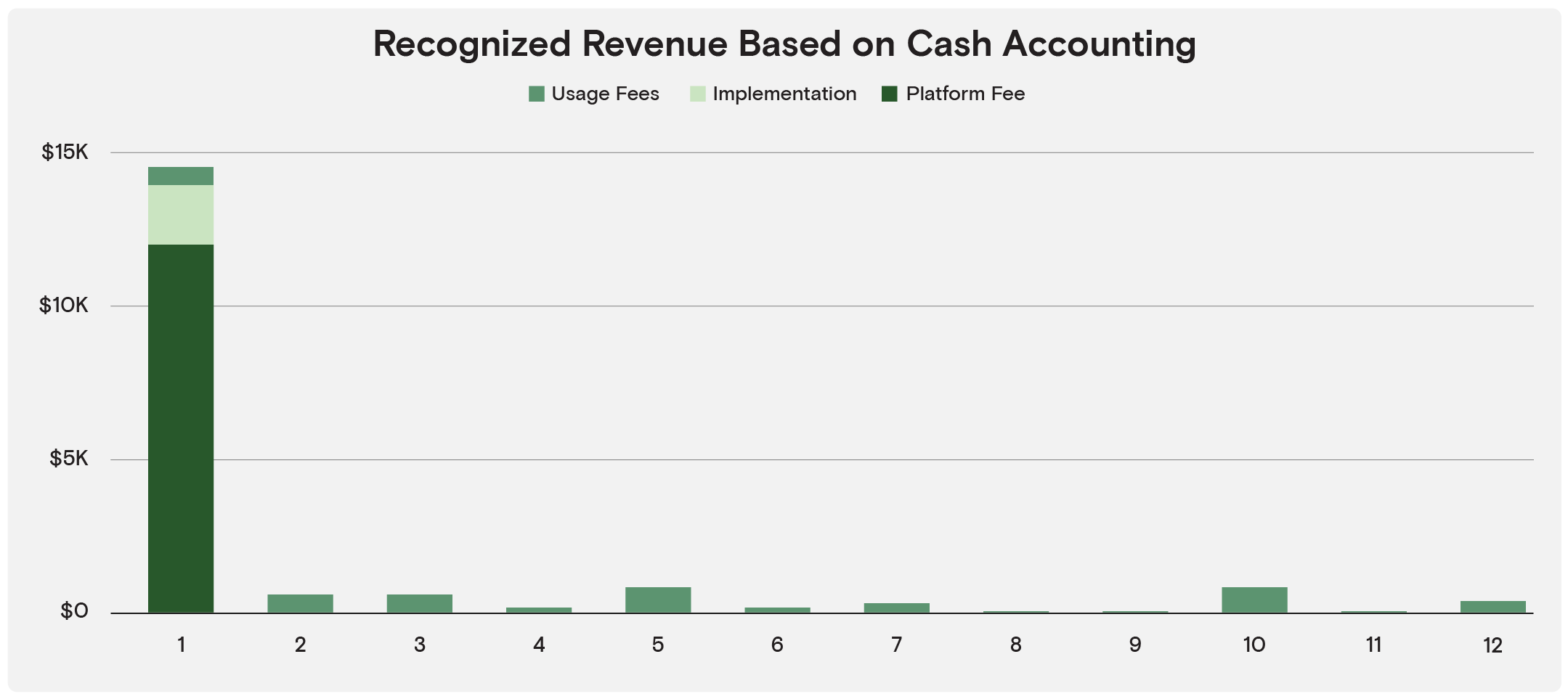

Compare the above chart to how the revenue would be recognized with cash accounting (see below). What the below chart is missing is that more than 75% of the revenue (cash) received in m1 has not been earned, and the costs associated with earning that revenue, which will be spread out over the term of the contract, are not easily tied back to revenue earned, complicating profitability metrics.

The ASC 606 process for recognizing revenue (or a close variant) is what buyers will expect to see when evaluating your company, so if you’re not currently employing this methodology, you will want to start the process.

Recognize Revenue the Way Buyers Expect You To

Before you enter into negotiations with a potential buyer, you need to make sure you have your house in order in terms of revenue recognition. If you have interested buyers already knocking at your door, the sooner you can apply this methodology, the better.

Properly recognizing revenue is a key aspect of how we prepare our clients for an M&A or capital raise transaction. To learn more about going through a transaction with an investment bank, check out the For Founders: The M&A Process section of our site.