2021 COVID-19 Impact on SaaS Valuations & Transactions

- How SaaS valuations have responded to the COVID-19 climate

- Why M&A transactions fell then recovered in the second half of 2020

- Why 2021 could be a good year for SaaS founders to run an M&A or capital raise transaction

In the last decade and a half, many software companies have made a bet on the SaaS model, trading in the large licensing fees of traditional software models for subscription revenue.

Until the pandemic, SaaS had always been a good bet—since the model first became popular, SaaS companies had consistently traded up compared to legacy software players. But in most cases, growing SaaS companies had never passed through a significant recession, the last occurring in 2008. So when the 2020 pandemic and economic shutdown began, founders and investors found themselves asking "Will SaaS companies be able to shore up retention rates?"

The short answer: yes. In many cases, SaaS companies more than survived the initial economic drop of the recession. For many publicly traded SaaS companies, years of technology adoption happened in months. Rapid adoption and associated revenue growth pushed valuations to an all-time high. Founders who have benefited from these circumstances should be asking themselves, "Given high valuations for SaaS, is now a good time to pursue a transaction?"

M&A Conditions Under the COVID-19 Pandemic

A perfect storm of founder-friendly economic conditions makes the mid-pandemic climate of 2021 optimal for many SaaS founders and shareholders to pursue an exit:

- Valuations are at an all-time high for SaaS companies achieving strong recurring revenue growth and KPIs

- Technology M&A made a full recovery in the second half of 2020, and strategic buyers are looking to M&A as an inorganic growth strategy to reach target metrics

- Private equity firms that closed their wallets in early 2020 now have large volumes of unallocated capital and they’re urgently looking for great assets

- Other factors, such as government stimulus programs and low interest rates have resulted in cheap debt and a flight to riskier, higher-yielding assets

Founders should evaluate each of the above conditions in turn to better understand the M&A implications for their own SaaS company.

Why SaaS Valuations Are Soaring Mid-Pandemic (and Why That Should Continue Post-Pandemic)

The strongest argument in favor of pursuing a transaction under current conditions comes from the outsized valuations SaaS companies are currently experiencing in the market.

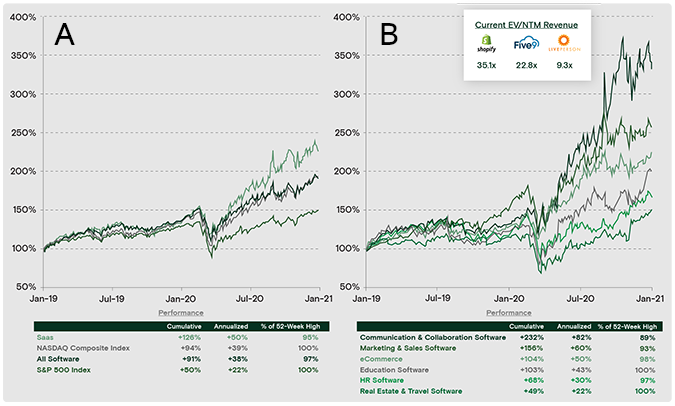

Despite a substantial bear market between late February and late March of 2020, the market as a whole rebounded with a vengeance. The rebound was even more pronounced for SaaS businesses—Vista Point Advisors’ SaaS index returned 90% between March 20th and the end of 2020, compared to the Nasdaq Composite Index 87% return (see Figure 1A).

Returns for best-of-breed assets operating in high-performing, COVID-insulated sectors (such as communications & collaboration, marketing & sales, eCommerce, and EdTech) were even more impressive and companies in these categories should continue to earn substantial forward revenue multiples (see Figure 1B).

Figure 1: SaaS rebounds more aggressively in H2 2020 compared to the general market

Source: Pitchbook 1/31/2021

The success of SaaS can be attributed to the following qualities:

SaaS companies that weathered the pandemic are positioned as "recession-proof" assets

For SaaS businesses founded after 2008, the pandemic represented the first opportunity to test how recession-proof and "mission critical" their product offering really was.

SaaS businesses that survived and maintained positive growth and customer retention trends amid COVID-19 conditions positioned themselves as critical for conducting business. As such, these businesses now attract the same or higher revenue multiples than they did pre-COVID due to greater perceived resilience and a scarcity of quality assets.

Longer-term contracts with fewer renewal periods

Even for SaaS companies that weren’t necessarily mission critical to business operations, contracted subscription revenue (not subject to cancellation and where renewal dates didn’t fall within the darkest hours of COVID fallout) acted as a saving grace.

Efficiency

The goal of software in general is to improve efficiency, but SaaS companies were especially positioned to do so under COVID conditions. Since SaaS and the Cloud are two sides of the same coin, a transition to work- and learn-from-home lifestyles didn’t dramatically limit access to software. If anything, cloud-hosted SaaS is what enables companies to continue business operations with 43% of the workforce at home.

CAPEX vs. OPEX

Because SaaS subscriptions are considered an operational expense (OPEX) rather than a capital expense (CAPEX), allocating budget is much easier than with license-based software instances, which are multi-year assets that need to be allocated budget directly out of the balance sheet.

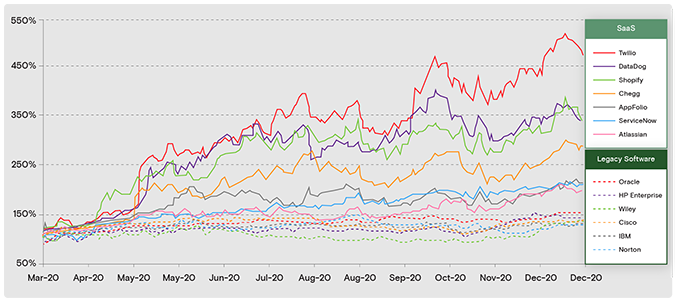

Consequently, SaaS companies that were already outpacing legacy software giants in terms of stock performance before the pandemic only further pushed away from legacy players like Oracle, HP Enterprise, Wiley, Cisco, IBM and Norton (see Figures 2 and 3).

Figure 2: SaaS vs. legacy software stock return performance

Source: Pitchbook March 16, 2020 to December 31, 2020

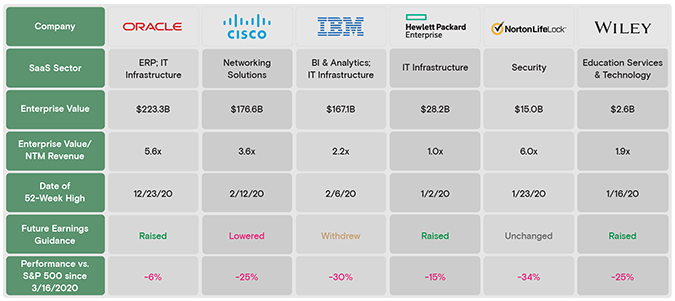

Figure 3: Legacy software providers experienced low valuation multiples and sub-par performance compared to the S&P 500 Index

Source: Pitchbook 12/31/2020

Will high valuations continue?

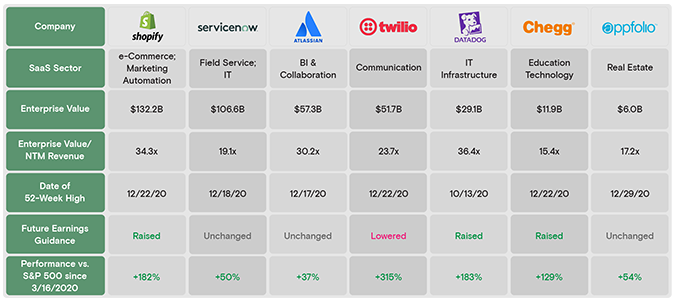

Well-positioned SaaS companies have thrived in the public markets in terms of valuation, as represented in Figure 4 and the following highlights:

- Shopify, Datadog, and Atlassian were all valued at >30x NTM revenue at the end of December 2020

- Twilio returned 315% over the S&P 500 between March and December 2020

This return and valuation multiple gap is likely to continue post-pandemic, as the software businesses that suffered during a work- and learn-from-home environment will be further left behind as the effects of the COVID-19 pandemic permanently shift future productivity patterns. As such, investors will continue to turn their attention to SaaS and away from other opportunities.

Any SaaS company that withstood or even thrived amid the pandemic will send strong signals to investors that their company is a desirable potential investment. And investors are again prepared to transact, despite a lapse in early 2020.

Figure 4: Well-positioned SaaS businesses continue to thrive on the public markets

Source: Pitchbook 12/31/2020

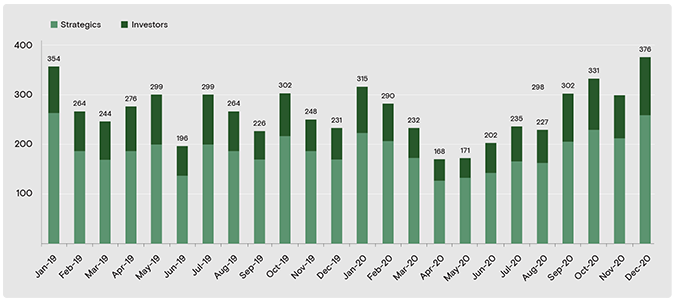

Technology M&A Made a Full Recovery in H2 2020

Transaction volume experienced unprecedented slowdowns during initial COVID-19 stay-at-home orders in March and April 2020, primarily as a result of massive market volatility and an inability on the part of M&A buyers to carry out normal diligence activities.

M&A conditions have since recovered. Summer 2020 first showed signs of recovery and Q4 2020 fully rebounded, with a 29% increase in deal volume versus Q4 2019 (see Figure 5). Matching with our expectations, and echoing the V-shaped public market recovery, tech M&A recovered in the second half of 2020 and reached an all-time high for the entire year.

Figure 5: Technology M&A transactions by month by buyer type

Source: Pitchbook 12/31/2020

The artificial slowdown caused by uncertainty surrounding COVID-19 created pent-up demand for SaaS businesses, which translated into increased deal volume in H2 2020 and 2021. Among the many prominent acquisitions of H2 2020 are:

- Twilio’s $3.2B acquisition of customer data platform Segment in November

- Salesforce’s $27.7B acquisition of SaaS communication platform Slack in early December

- Intuit’s $7.1B acquisition of CreditKarma in early December

- Large PE take-privates of names such as RealPage, Pluralsight, LogMeIn, Benefytt Technologies, and MobileIron

The acceleration of M&A is in part fueled by an increase in strategic buyers’ stock prices, creating valuable currency for acquisitions. Large strategic buyers such as Facebook, Amazon, Google, Microsoft, Salesforce, Adobe, Twilio, NVIDIA, AMD, etc., have seen their stock prices rise dramatically and have used this more valuable currency as fodder for acquisitions. Consider:

- Salesforce’s acquisition of Slack for $27.7B (the largest enterprise software M&A deal ever)

- AMD’s $35B merger with Xilinx and NVIDIA’s $40B acquisition of Arm—two of the largest-ever semiconductor deals (both announced in 2020 but currently subject to regulatory approval)

In addition, as growth stalled due to COVID-19 fallout, many strategic buyers are looking to M&A as an inorganic growth strategy to make up for shortcomings in organic growth. On the private equity & venture capital side of M&A, an excessive supply of dry powder has investment firms feeling urgent to close transactions and willing to pay premiums (more on this below).

With M&A activities again open for business, founders are able to entertain interested strategic buyers and investors for a potential acquisition or capital raise.

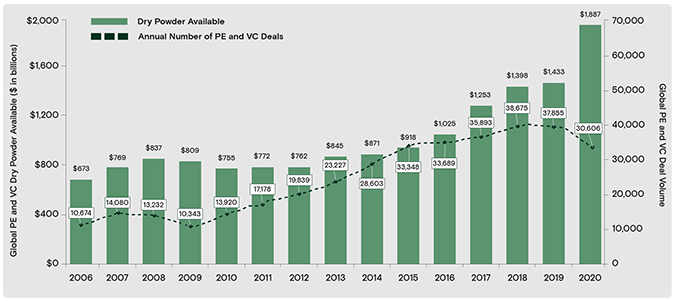

PE/VC Dry Powder Without a Home Remains at Staggering Levels

With a cumulative $439B in capital raised by PE and VC funds from Q2 through Q4 of 2020, investment firms had high expectations for 2020 and beyond. Now they’re urgently looking to place that capital in the best businesses.

As a result of the onset of COVID-19, the number of transactions completed in 2020 experienced a 19% YoY decline from 2019. Due to the slower than expected deal volume in the first half of 2020, PE/VC firms have a surplus of capital waiting to be deployed (see Figure 6).

As investment firms have tightened their criteria for transacting, fewer businesses fit the bill. At the same time, investors still have $1.9T of estimated dry powder as of year-end 2020. As such, for those companies that have proved resilient to the downturn, there is a perfect storm brewing for continued high valuations in private markets in 2021 and beyond.

Figure 6: PE & VC dry powder remain at all-time highs

Source: Pitchbook 12/31/2020

Another effect of PE firms' ample dry powder is that PE firms are eager and financially capable to close on expedited timelines with remote meetings and third-party diligence providers—a boon for founders. In addition, processes have become even more competitive as PE buyers have developed proprietary "playbooks" that allow portfolio companies to grow through the pandemic and increase equity value.

Large take-privates exemplify how endless dry powder coupled with low-interest debt have resulted in elevated valuations:

- Francisco Partners acquired LogMeIn for $4.3 billion, a 25% premium to the September 18, 2020 closing share price

- Thoma Bravo acquired RealPage at a 31% premium to the December 18, 2020 closing stock price

- Vista Equity acquired Pluralsight at a 25% premium to 30-day VWAP

Other Factors Improving Conditions for an M&A Transaction or Capital Raise in 2021

Other important conditions (listed below) further position 2021 as a strong year for founders to pursue a transaction.

Government stimulus programs have helped mitigate risk

Since the general slowdown in Q2 2020 (due to uncertainty around unemployment rates, travel restrictions, bank liquidity, and money markets), massive government stimulus programs like the Paycheck Protection Program, Economic Impact Payments, and quantitative easing have allowed capital to flow back into risk assets.

COVID-19 accelerated growth for certain SaaS sectors

Cloud-based platforms for remote collaboration, learning, field services, events, and entertainment have seen a net benefit from the pandemic. A decade of technological adoption and implementation took place over nine months in 2020.

Even in a post-COVID world, we expect a "hybrid economy" to develop which features both remote and in-person elements. Virtual/remote commerce, communication, business workflow, events, and other technological shifts appear set to continue.

COVID-19 made M&A more competitive for non-resilient sectors

As certain sectors have struggled through COVID-19 (e.g. retail, travel, hospitality) there is more capital chasing an even fewer number of viable investment opportunities. To illustrate, consider Thoma Bravo’s $10.2B acquisition of RealPage and the myriad other travel and real estate-related transactions even as those industries are largely dormant.

The Opportunity Has Never Been Better for Software Exits

Overall, in a climate of strong uncertainty, investors are looking at sticky SaaS companies to minimize that uncertainty, making the present conditions an exceptional time to pursue a transaction.

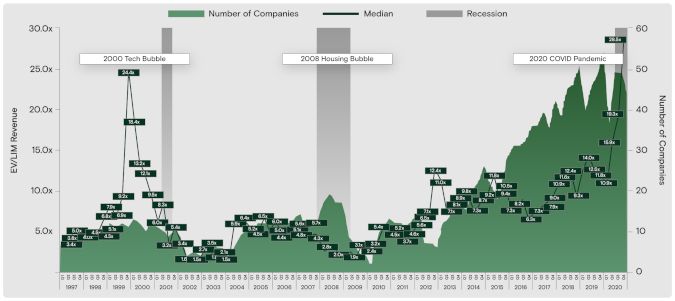

Multiples for SaaS companies are higher than ever before (see Figure 7) and are likely to stay that way in the near-term as the pandemic continues to favor SaaS offerings—specifically COVID-insulated ones.

Figure 7: Valuation multiples (Median Enterprise Value / LTM Revenue) for >30% LTM Revenue Growth public software companies

Source: Pitchbook 12/31/2020

In early 2021, SaaS companies are valued at a premium, M&A activity has grown despite limitations imposed by the pandemic, and private equity firms have an excess supply of capital to invest at low interest rates. Under the current conditions, founders of software companies should seriously consider pursuing a transaction in 2021 for an outsized exit.